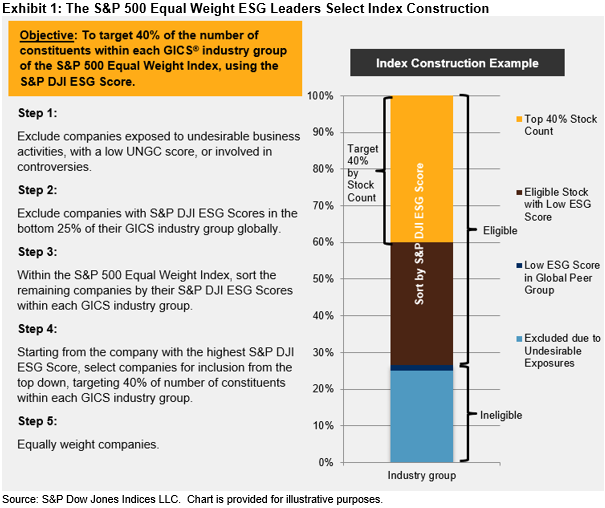

“Code red for humanity.” That’s how the imminent effects of climate change were described by the UN.1 Human-induced global warming stands at 1.1°C above pre-industrial levels, and will likely reach more than 2.7°C by 2100.2 If the world is to achieve the goals of the Paris Agreement and limit global warming to 1.5°C, decarbonization is the answer. The S&P PACTTM Indices (S&P Paris-Aligned & Climate Transition Indices) aim to align with the Paris Agreement goals and be compatible with net-zero emissions by 2050.

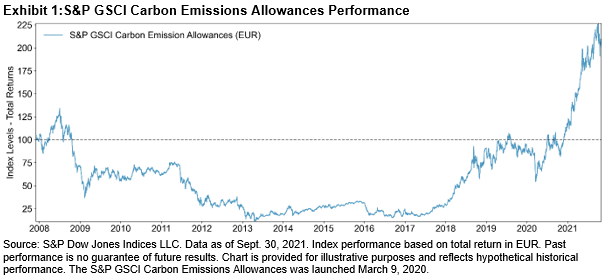

Carbon pricing encourages companies to reduce greenhouse gas (GHG) emissions, accelerating the transition to a low-carbon economy. Growing carbon prices have been observed within the EU Emissions Trading Scheme, whose price has surged 126.58% in one year.3

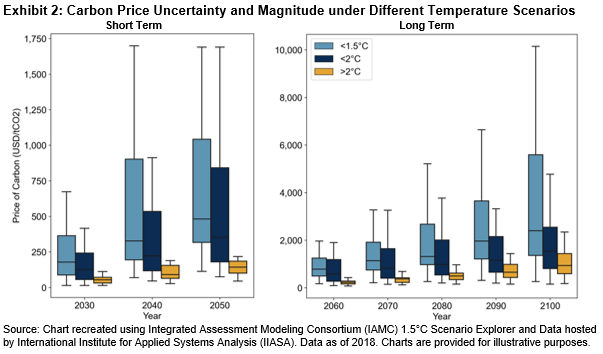

To curb global warming to 1.5°C, carbon prices would likely need to increase dramatically over the upcoming decades, much more than if that target were pushed to above 2°C. However, the uncertainty surrounding that increase is huge. Naturally, this translates into potential financial risk, as companies would have to either absorb the additional cost of their carbon emissions or pass it on to consumers—the so-called carbon price premium.

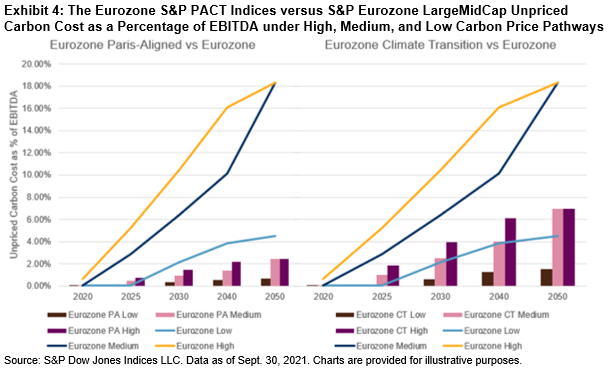

Using S&P Global Trucost’s Carbon Earnings at Risk dataset, we test whether the eurozone S&P PACT Indices show more financial resilience to a growing carbon price, or rather, if we observe lower portfolio earnings at risk, relative to its benchmark. Trucost developed the following three carbon price pathways.

- Low carbon price reflecting countries’ NDCs4

- Medium carbon price assuming a 2°C goal, but with short-term action delayed

- High carbon price aligned with the 2°C goal of the Paris Agreement

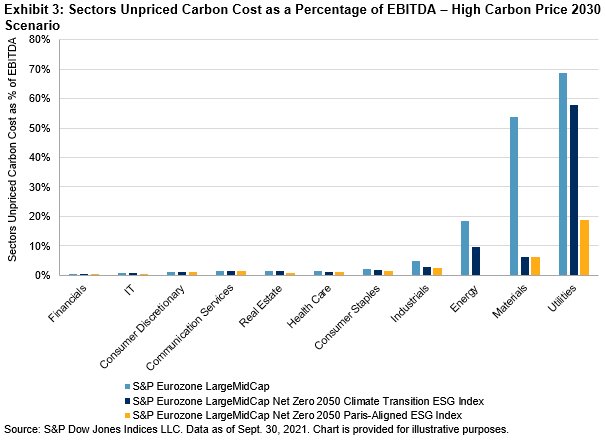

Sectors have different exposures to this transition risk, with Utilities and Materials being some of the most vulnerable to soaring carbon prices, given their operational nature.5

We examine the proportion of the eurozone S&P PACT Indices earnings at risk from potential rising carbon prices, as a percentage of earnings before interest, tax, depreciation, and amortization (EBITDA). Both the S&P Paris-Aligned (PA) Index and S&P Climate Transition (CT) Index carbon earnings at risk were lower than the underlying S&P Eurozone LargeMidCap under each scenario from 2020 to 2050.

If the world aligns with the Paris Agreement goals and adopts a high carbon price (shown by the dark purple bars and yellow lines), that implies both the PA and CT indices have 8.99% and 6.50% less portfolio earnings at risk by 2030 relative to their underlying index, respectively.6 When looking at 2050, that increases to 15.86% and 11.36%.

Trucost’s models suggest that the eurozone S&P PACT Indices are more financially robust on a forward-looking basis than their underlying market-cap-weighted index. The magnitude of their potential climate resiliency would be dependent on the specific climate trajectory the world ends up pursuing.

1 UN Secretary-General António Guterres’ statement on the Intergovernmental Panel on Climate Change (IPCC) Working Group 1 report on the physical science basis of the sixth assessment, available here.

2 Based on the Nationally Determined Contributions (NDCs)and pledges submitted as of 2020, the world is on track for 2.7°C of warming, according to the contribution from Working Group I on the IPCC AR6 Report: Climate Change 2021: The Physical Science Basis.

3 As of Sept. 30, 2021.

4 NDCs form the basis for countries to achieve the objectives of the Paris Agreement. They contain information on targets, policies, and measures for reducing national emissions and on adapting to climate change impacts (UNFCC, 2021).

5 Please note Trucost’s Carbon Earnings at Risk dataset only includes Scopes 1 and 2 of GHG emissions.

6 All data as of Sept. 1 2021.

The posts on this blog are opinions, not advice. Please read our Disclaimers.