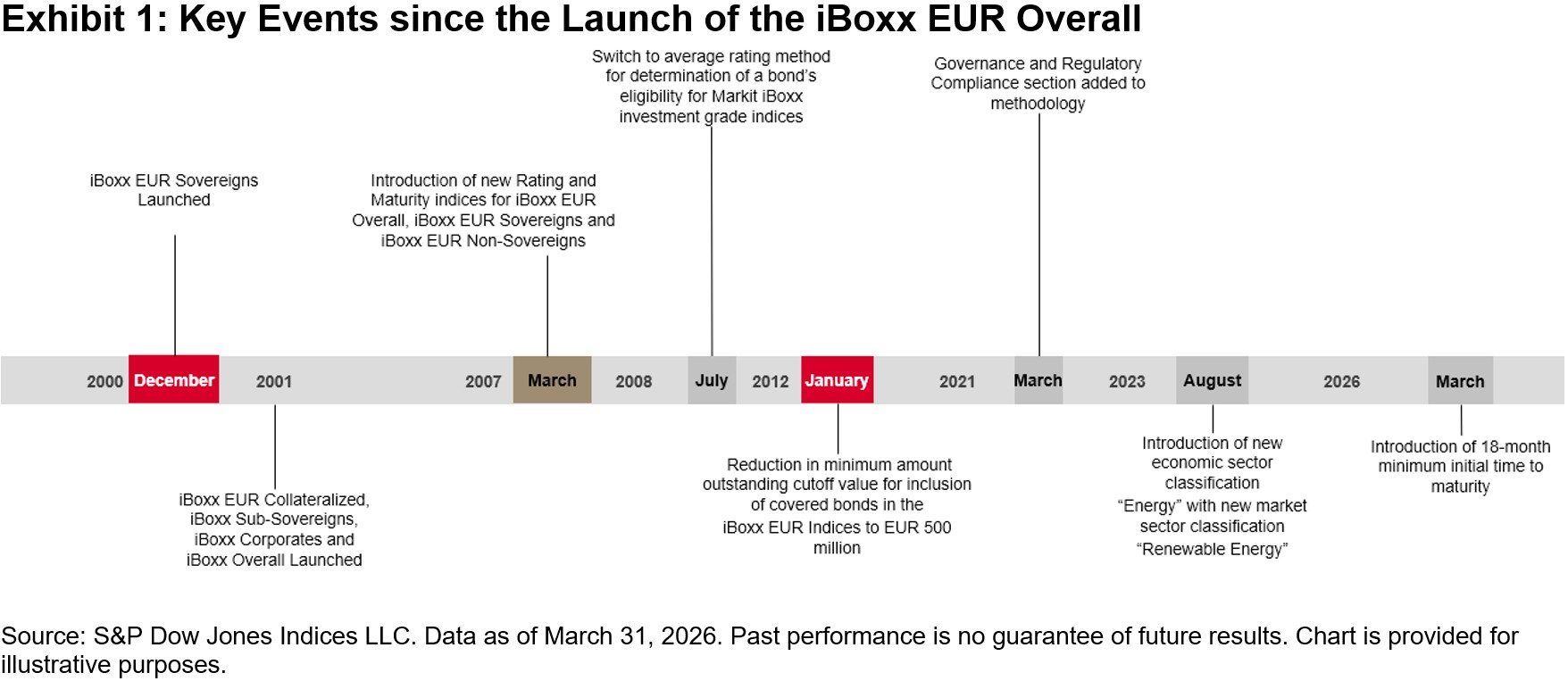

Over the past 25 years, the iBoxx EUR indices have evolved alongside the market they were built to measure (see Exhibit 1).

The journey began in 2000 with the launch of the iBoxx EUR Sovereigns, at a time when the eurozone bond market was still taking shape and investors were looking for transparent benchmarks. As the market expanded, new building blocks followed, including the iBoxx EUR Collateralized, iBoxx Sub‑Sovereigns and iBoxx Corporates. These eventually came together under the iBoxx EUR Overall, which was introduced to provide a single view of the EUR‑denominated bond universe.

A turning point came in July 2012, during the eurozone sovereign crisis. Disagreements between rating agencies were creating volatility and liquidity concerns, and the use of the lowest rating in index rules amplified these issues. The switch to an average rating was introduced to address this, offering a more balanced and stable way of assessing credit quality within the indices.

Another step in the evolution arrived in August 2023 with the introduction of a dedicated renewable energy sector classification. This reflected both the rapid growth in issuances linked to renewable energy projects and the shift in investor focus, supported by policy changes such as the EU raising its 2030 renewable energy target from 32% to 45%.1, 2, 3 Recognizing renewable energy as its own sector ensured that the indices reflected a part of the market with distinct characteristics, risk profiles and growing strategic importance.

The most recent development came in March 2026, when an 18‑month minimum initial time to maturity was introduced to align the iBoxx EUR indices with industry practice and remove short‑dated bonds that offered limited contribution to the index profile.

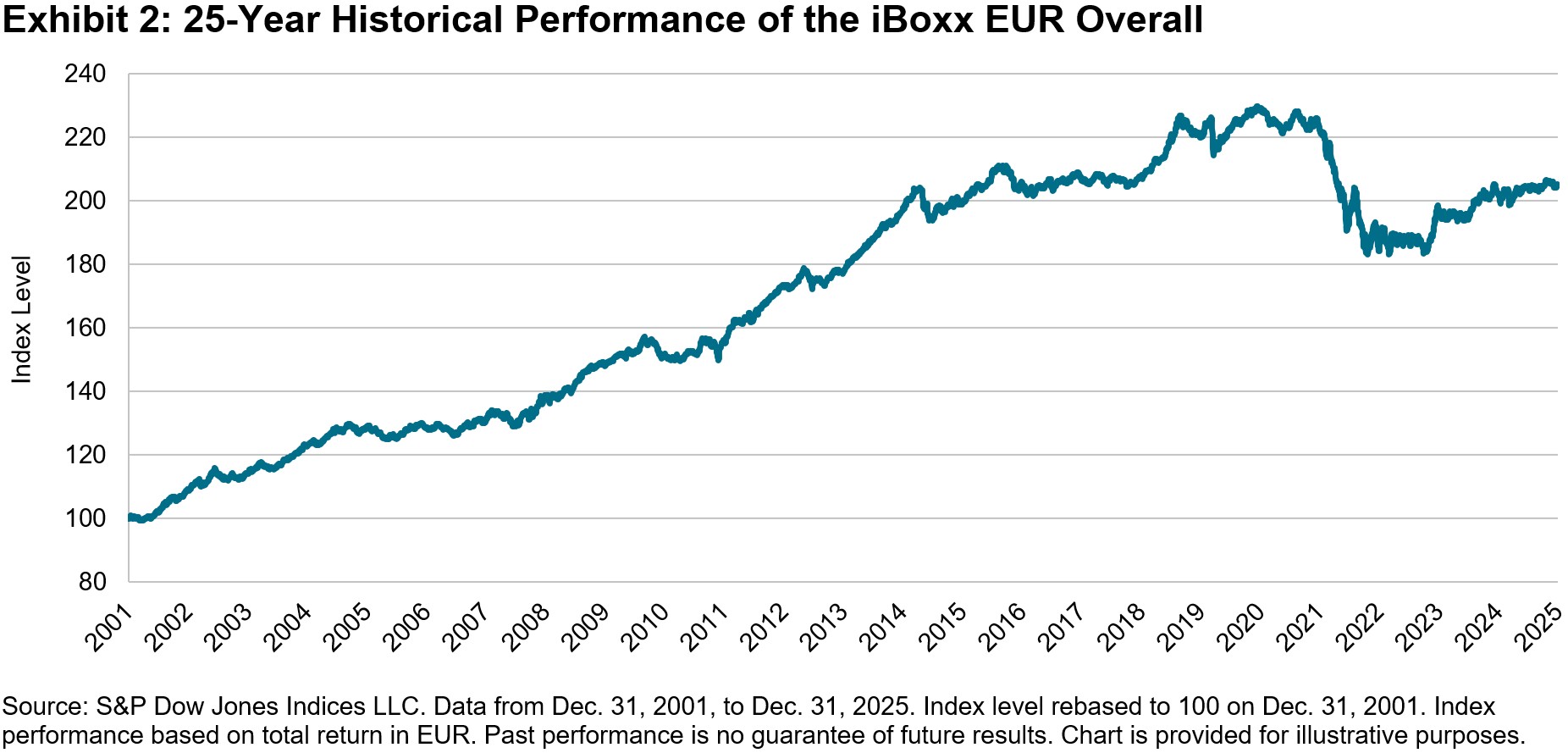

The long-term performance of the iBoxx EUR Overall illustrates how the index has changed over 25 years of shifting market conditions (see Exhibit 2).

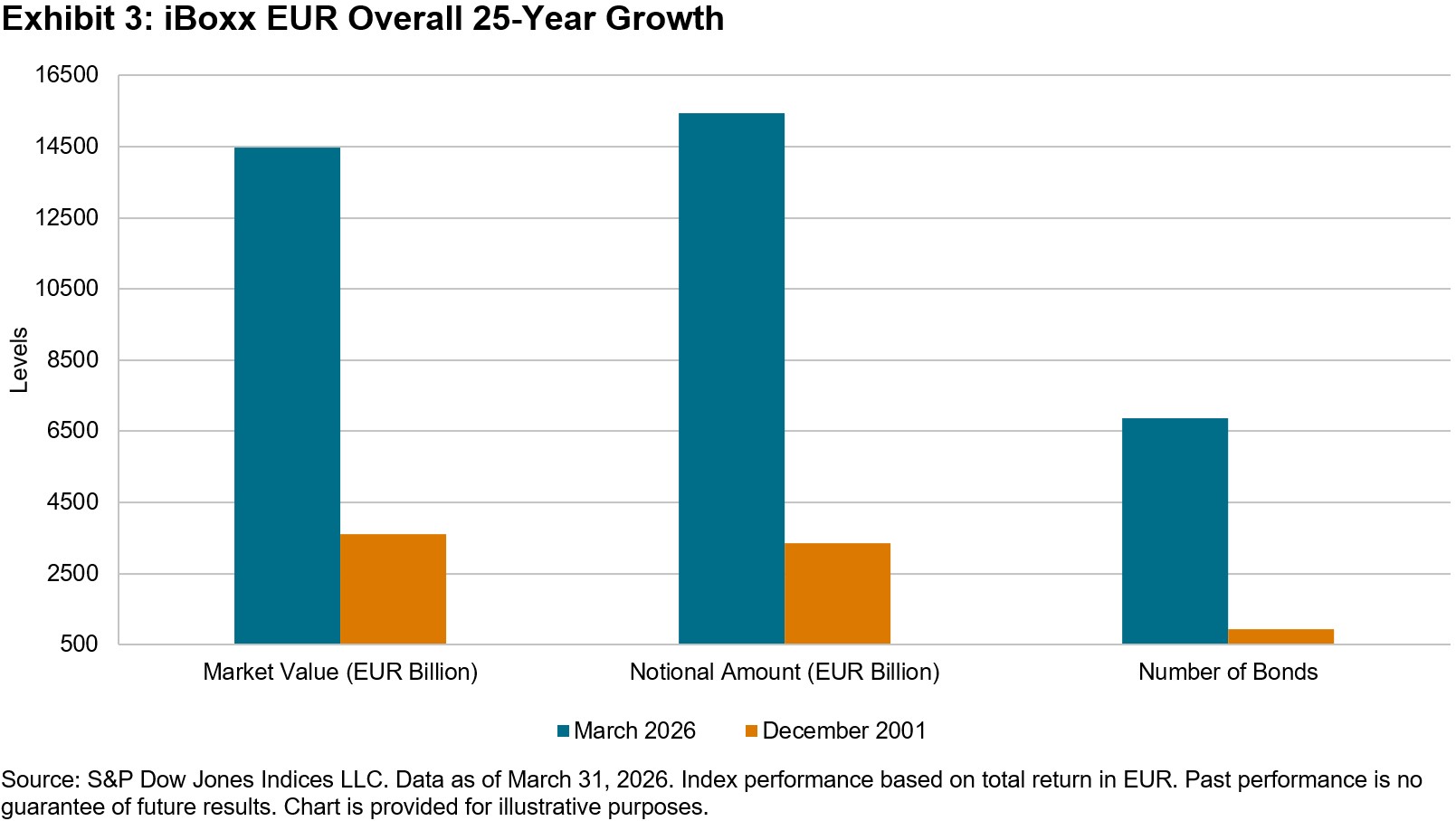

Market size and issuance have grown increasingly over the past 25 years (see Exhibit 3). As the iBoxx EUR indices expanded to reflect larger segments of the investable market, this growth reflected a series of major macro events, including quantitative easing, the sovereign debt crisis and the broader influence of central bank policy. The iBoxx EUR Overall index has grown alongside these developments, both responding to them and being shaped by the shifts in liquidity, yields and issuance patterns that followed.

The rise in notional amounts highlights not only the increase in issuance and market liquidity, but also the expansion of ESG and green bonds, the development of new corporate sub-sectors and the inclusion of a wider range of bond types. As the investable universe broadened and investor demand increased, fixed income indexing evolved to incorporate these instruments, ensuring that the indices reflected a larger and more diverse portion of the market with meaningful growth potential.

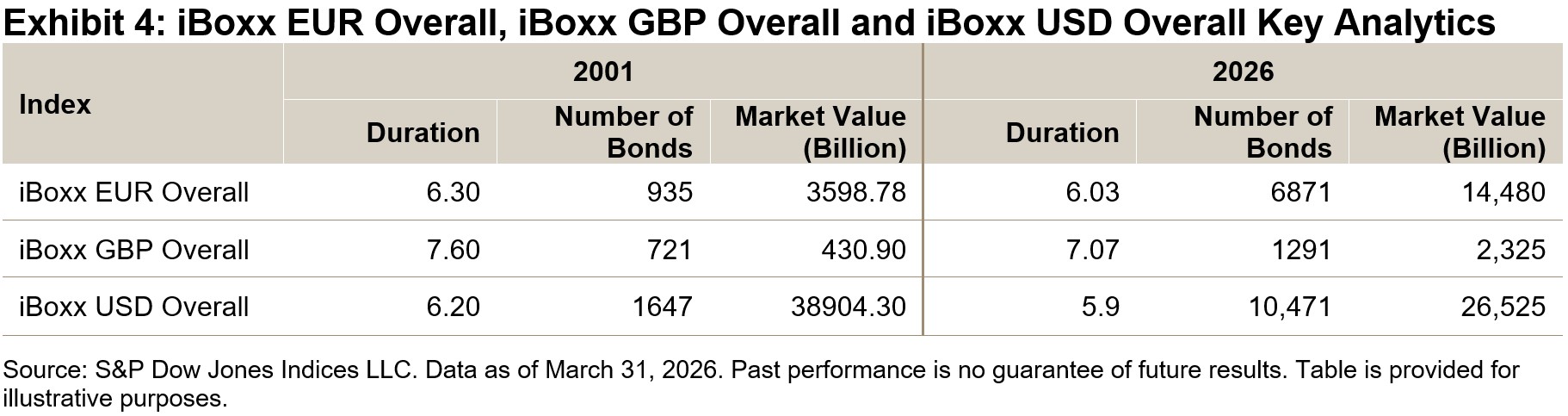

We see duration shorten across other key index series including the iBoxx GBP Overall and iBoxx USD Overall, reflecting a market that has steadily moved toward shorter maturities (see Exhibit 4). Repeated macro shocks, post‑crisis regulation and the shift away from years of unusually low rates pushed issuers to favor shorter, more flexible borrowing, and fixed income indices have naturally followed as the composition of the investable universe has shifted.

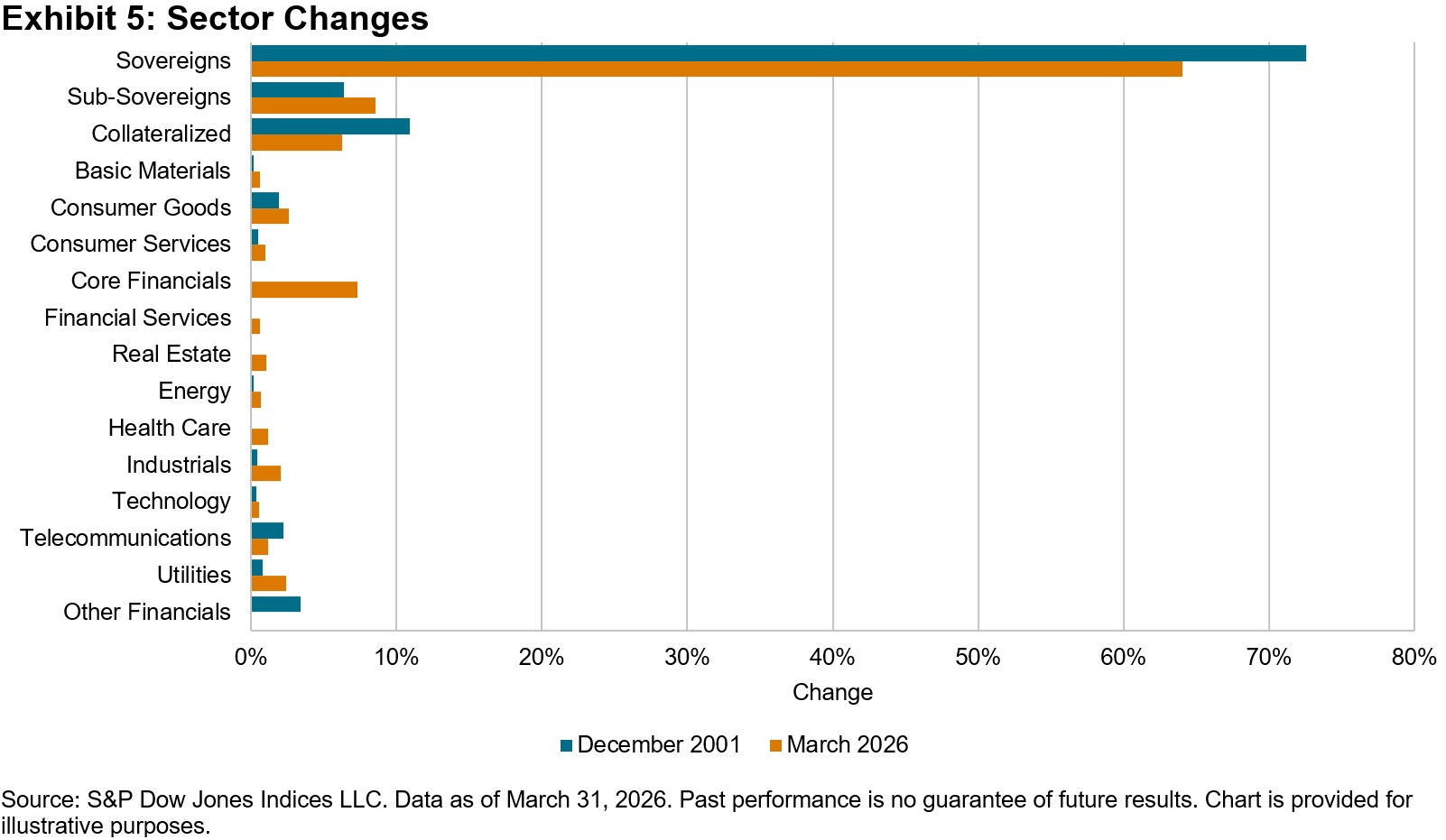

The iBoxx EUR series began with a strong focus on sovereigns, and this is reflected in the early composition of the index, where sovereigns accounted for 73% of the universe in 2001. Over time, this dominance eased to 64% in 2026 as new and more specialized corporate subsectors began to emerge. As the market broadened, the index evolved into a more diversified and representative view of the investable EUR bond universe.

We see the appearance and gradual growth of corporate subsectors such as Technology, Energy, Real Estate and Health Care (see Exhibit 5). These developments coincided with several structural shifts in the market: the rise of REITs issuing EUR debt, increased capital‑raising from Technology firms as cyber- and AI‑related investment accelerated, and the expansion of the Energy sector as renewable energy developers issued bonds to finance large‑scale infrastructure projects. Together, these changes reflect how the index adapted to reflect new sources of issuance and the evolving shape of the European economy.

The additional financial classifications are particularly notable. Following the 2008 Global Financial Crisis, regulation reshaped the Financial Services sector and exposed the need for clearer distinctions between different types of issuers. As banks, insurers and other financial institutions issued increasingly varied forms of debt, the index methodology evolved to separate these categories, improving the accuracy and relevance of sector representation.

The past 25 years highlight how fixed income indexing has evolved with changes in market structure. Looking ahead, infrastructure investment, hyperscalers, data‑center expansion, emerging corporate subsectors and the shift of private‑market‑style structures into public markets are all likely to guide how classifications, subsectors and bond‑type coverage develop, and the iBoxx indices will continue to evolve to reflect these themes as they take shape.

1 “Renewable energy,” Fact Sheets on the European Union. European Parliament.

2 “EU Market Outlook for Solar Power 2023-2027.” Solar Power Europe, Dec. 12, 2023.

3 For more information, please see the iBoxx EUR Benchmark Index Methodology.

The posts on this blog are opinions, not advice. Please read our Disclaimers.