In the U.S. market, options-based ETFs have experienced exponential growth in recent years, with total assets reaching USD 245 billion as of December 2025. These strategies have been increasingly adopted as mainstream tools in portfolio construction, offering more predictable outcomes and income diversification.

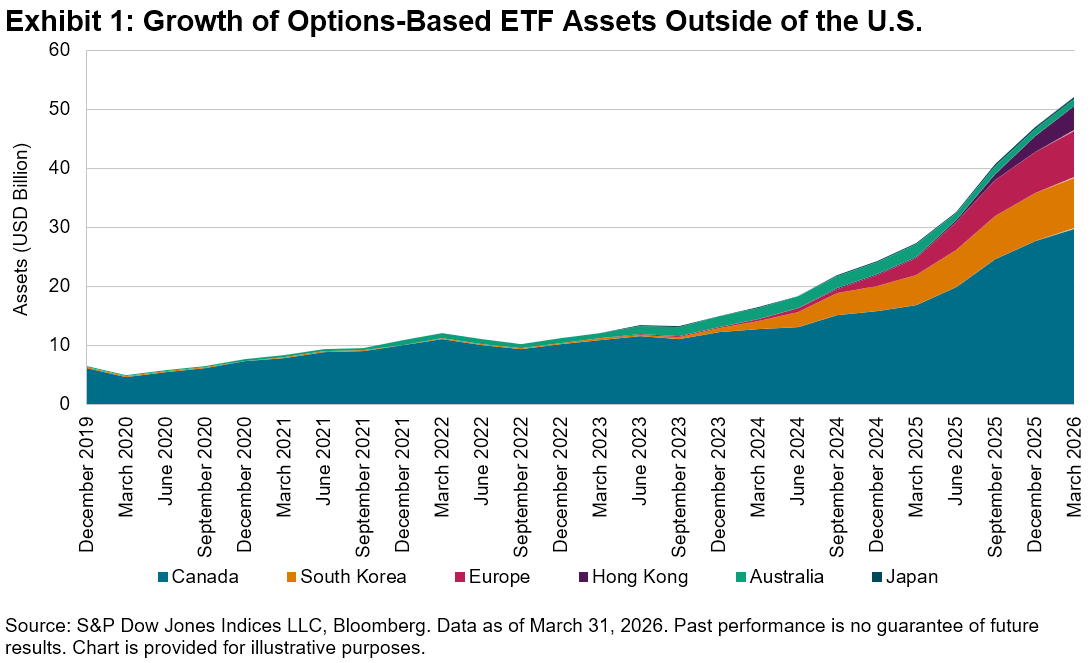

Other regions are catching up with this trend at varying rates, with some accelerating rapidly while others are adapting regulations to allow this segment to grow in their local markets. Canada is by far the largest market outside of the U.S., with options-based ETF assets totaling USD 30 billion as of March 2026, followed by South Korea (USD 9 billion) and Europe (USD 8 billion). Hong Kong has also seen rapid expansion, accumulating over USD 4 billion in assets since the debut of its first covered call ETF in early 2024.

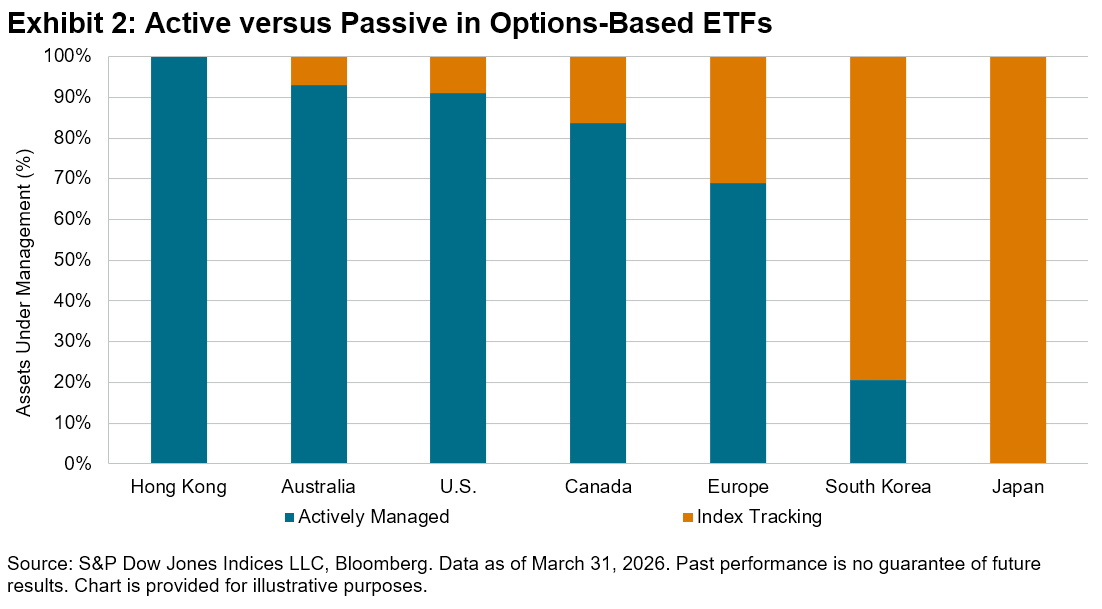

While covered call strategies remain dominant in international markets, accounting for 92% of the total assets compared to 62% in the U.S., each market has developed distinct approaches to product design and management. In markets such as Hong Kong, Australia and Canada, options-based ETFs are largely managed actively, mirroring the U.S. where 91% of assets are actively managed.1 Conversely, in markets such as South Korea and Japan, most assets track options-based indices to provide targeted outcomes (see Exhibit 2).

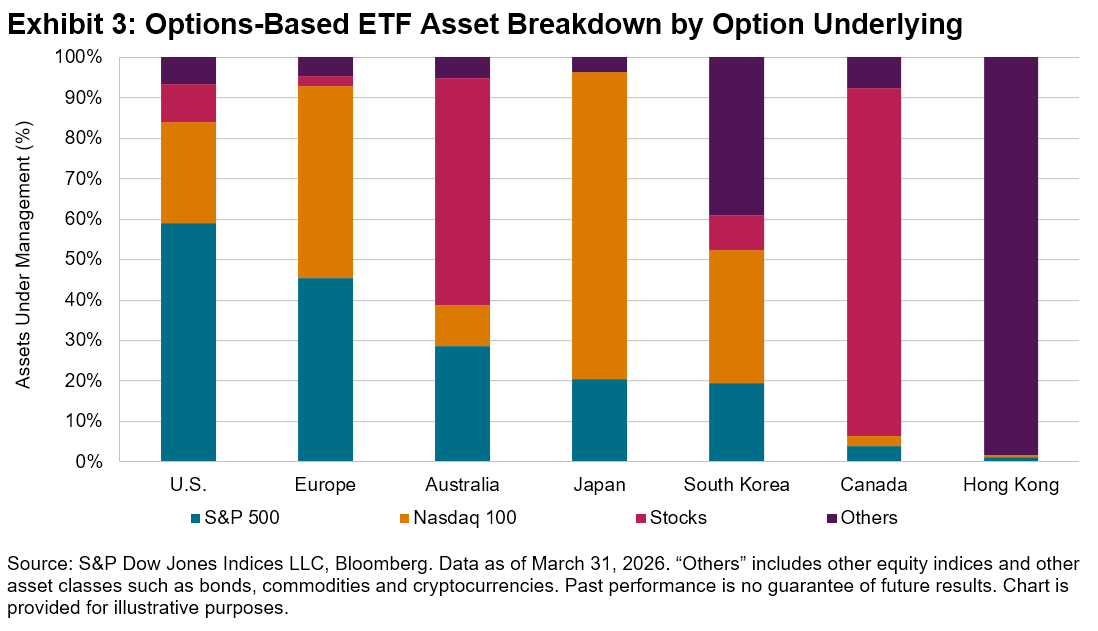

The underlying assets for options being used in ETFs also vary. U.S. benchmarks such as the S&P 500® and Nasdaq 100 are the most popular choices in Europe and Japan, while local indices dominate in Hong Kong. Single-stock options are prevalently used in Canada, while South Korea exhibits a relatively balanced distribution across U.S. indices, local indices, stocks and other asset classes (see Exhibit 3).

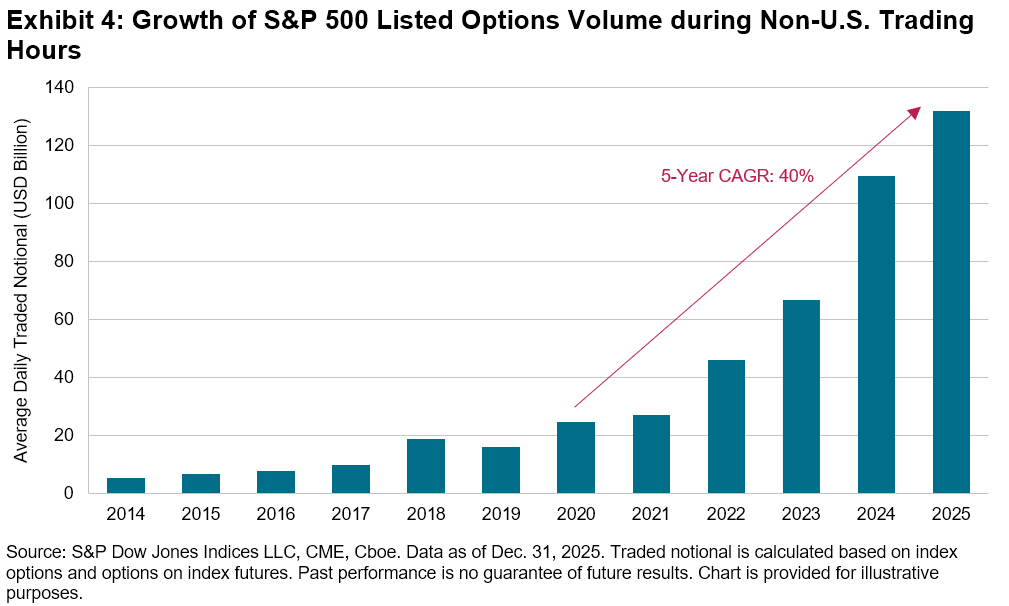

Notably, the S&P 500 remains a premier choice in many markets outside of the U.S., thanks to its unparalleled around-the-clock liquidity. These products often tap into the S&P 500 option liquidity2 outside standard U.S. trading hours. The non-U.S. trading hour3 liquidity has improved significantly, with average daily traded notional4 reaching USD 132 billion in 2025 (see Exhibit 4). This deep, continuous liquidity pool facilitates the effective implementation of various strategies based on S&P 500 options globally, catering to diverse investment objectives and preferences.

For a deeper dive into the index framework of options-based strategies, see “Defining Paths with Options-Based Index Strategies.”

1 Note that some ETFs are run in a manner that is notably different to traditional active management. For example, a fund described as active may exclusively use S&P 500-linked derivatives and exhibit performance very similar to an index representing the overall strategy.

2 See Edwards, Tim et al. “The Liquidity Landscape: Trading Linked to S&P DJI Indices,” S&P Dow Jones Indices.

3 Non-U.S. trading hour refers to 5:00 pm to 8:00 am Central Time for E-mini S&P 500 options and Micro E-mini S&P 500 options traded on CME and 7:15 pm to 8:25 am Central Time for S&P 500 Index options (SPX) and Mini-SPX Index options (XSP) traded on Cboe.

4 Dailly traded notional is calculated as index price x contract size x number of contracts traded for the day, with no delta adjustments.

The posts on this blog are opinions, not advice. Please read our Disclaimers.