Cybercrime’s AI Moment

Cybersecurity has recently entered the crosshairs amid advances in AI. The preview of Claude Mythos has raised concerns among government and industry officials about its broader implications for an increasingly digital economy. That growth in digital commerce has brought cybercrime with it, exploiting the anonymity and borderless nature of the web to grow in both scale and sophistication. Estimated at USD 220 billion globally, cybersecurity spending is forecast to grow 13% annually, underscoring the sector’s rising importance as AI reshapes the threat landscape.

Tracking Cybersecurity: Construction and Performance

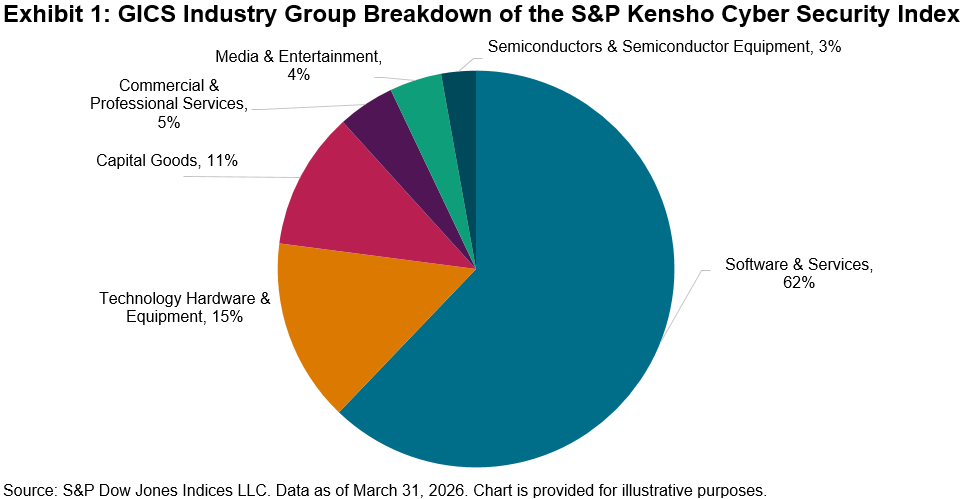

Given its significance to both today’s and tomorrow’s economy, Cyber Security is one of 25 themes within the S&P Kensho New Economies framework driving the Fourth Industrial Revolution. The S&P Kensho Cyber Security Index includes only companies whose primary business is cybersecurity, reflecting the sector’s depth and maturity.1

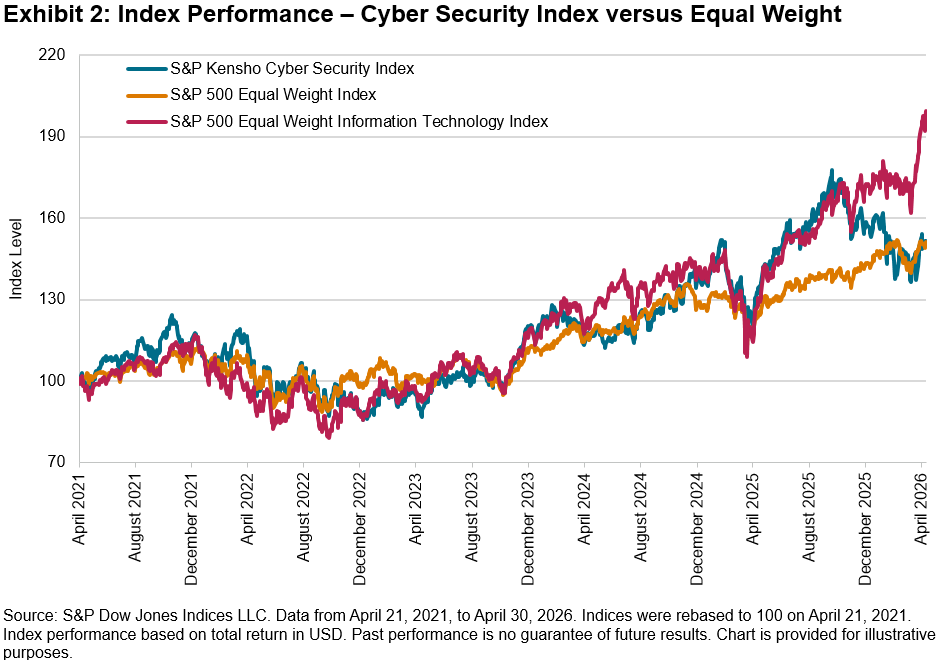

The S&P Kensho Cyber Security Index delivered a five-year annualized total return of 9%, in line with the S&P 500 Equal Weight Index, and outperformed it over the three-year period. A modified equal weighting methodology was chosen for the S&P Kensho Cyber Security Index to avoid the concentration risk that characterizes many technology-linked indices, and performance is therefore compared against equal-weighted benchmarks. Since peaking in October 2025 alongside the broader market, the index has churned to a flat YTD return and sits 13% below its historic high, as markets continue to weigh AI’s ultimate impact on the sector.

Dressed as Software, Built Like Defense

While cybersecurity is software by definition and closely correlated with Software & Services industry group, the segment makes a compelling case for greater resilience to AI disruption. Unlike much of the software world, cybersecurity spending is largely non-discretionary, underpinned by regulatory mandates that persist regardless of the economic cycle or technological change. Rather than a threat, AI may prove to be a catalyst. Expanding digital touchpoints widens the scope for malware attacks, driving demand for greater governance, compliance and protection. The net effect points to an expanding total addressable market for cybersecurity, with AI creating demand faster than it automates existing functions.

Cybersecurity and broader software indices have faced headwinds in recent months, while defense stocks have moved in the opposite direction, buoyed by rising geopolitical tensions. This divergence, however, may obscure a deeper connection, as governments across major economies now explicitly identify cybersecurity as a national security priority, blurring the line between digital and physical defense.2, 3, 4

Defense without Borders

Treating cybersecurity as an integral part of the broader security landscape, we track this theme through two complementary indices:

- The S&P Kensho Future Security Index5 takes a forward-looking view, positioning Cyber Security alongside Space, Robotics, Drones and Wearables as the technologies defining the future of the security landscape.

- The S&P Atlas Security, Defense, and Operational Support Index offers a ready-made group of constituents spanning the full security landscape across eight clusters, including Digital Security, Aerospace, Weaponry and Robotics, covering both established and emerging defense technologies. Constituents are selected globally using an AI/NLP framework developed by Theia Insights. The index forms part of the broader S&P Atlas Thematic Indices suite, designed to reflect both current and future drivers of a theme within a single diversified framework.

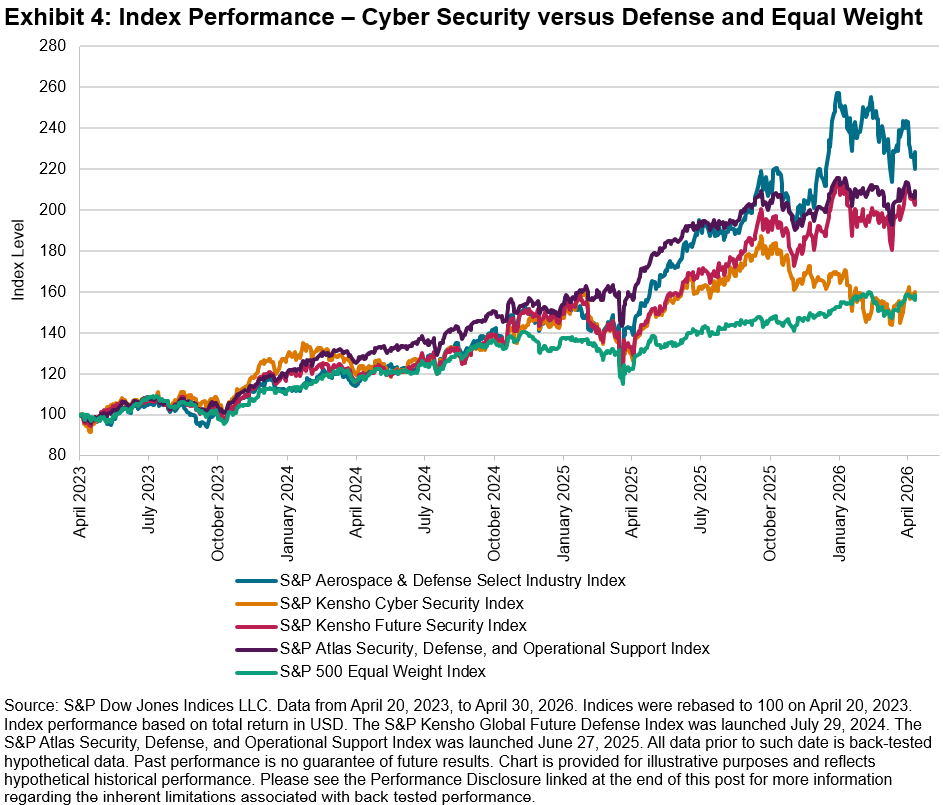

The S&P Kensho Future Security Index has delivered strong performance, posting a three-year annualized gain of 29%, slightly behind the S&P Aerospace & Defense Select Industry Index. The performance differential is partially attributed to the modified equal weight approach of the Kensho index relative to the float market cap weighting of the S&P Aerospace & Defense Select Industry Index.

The S&P Atlas Security, Defense, and Operational Support Index has taken a more balanced path over the same period, broadly tracking the defense theme while retaining cybersecurity as a core cluster. This reflects the blend of established defense and emerging security technologies that are included in the index.

Conclusion

Cybersecurity sits at a crossroads. AI has placed it under scrutiny as a software sector, yet simultaneously strengthened its case as a defense priority. As that tension plays out, the S&P Kensho Cyber Security Index, S&P Kensho Future Security Index and S&P Atlas Security, Defense, and Operational Support Index provide three ways to track this evolving theme, from pure-play cybersecurity to the full breadth of the modern security landscape.

1 The S&P Kensho Global Cyber Security Screened Index extends this benchmark to a global universe of companies, with an additional layer of sustainability-based eligibility criteria required for inclusion.

2 Shift in U.S. Cyber Strategy: What the White House’s New Offensive Cyber Posture Signals for Businesses. Baker Donelson. March 10, 2026.

3 NIS2 Directive: securing network and information systems, European Comission.

4 Outline of the Cybersecurity Strategy. National Cybersecurity Office, Japan. Dec. 23, 2025.

5 The S&P Kensho Global Future Defense Index extends this benchmark to a global universe of companies.

The posts on this blog are opinions, not advice. Please read our Disclaimers.