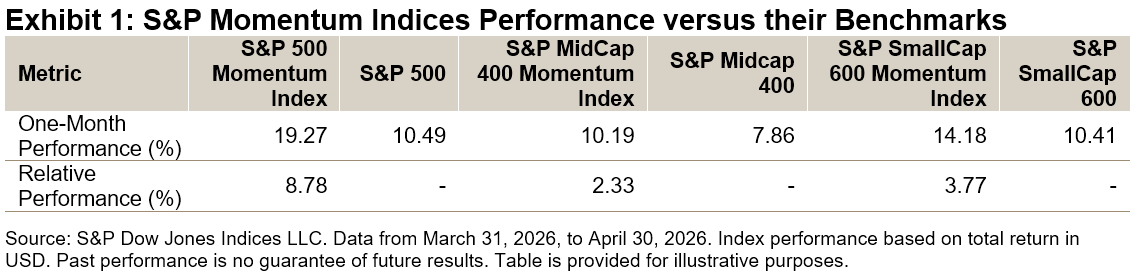

Momentum strategies, which tend to be known for performing well in trending markets, experienced a historically strong rebound in April. The S&P 500® Momentum Index, S&P MidCap 400® Momentum Index and S&P SmallCap 600® Momentum Index all posted double-digit gains, surpassing their respective benchmarks (see Exhibit 1). Notably, the April performance of the S&P 500 Momentum Index was the largest monthly gain since its inception in 1994.

In this blog, we will review the methodology, performance characteristics and attribution of the S&P Momentum Indices, with particular focus on the S&P 500 Momentum Index, S&P MidCap 400 Momentum Index and S&P SmallCap 600 Momentum Index.

Index Methodology

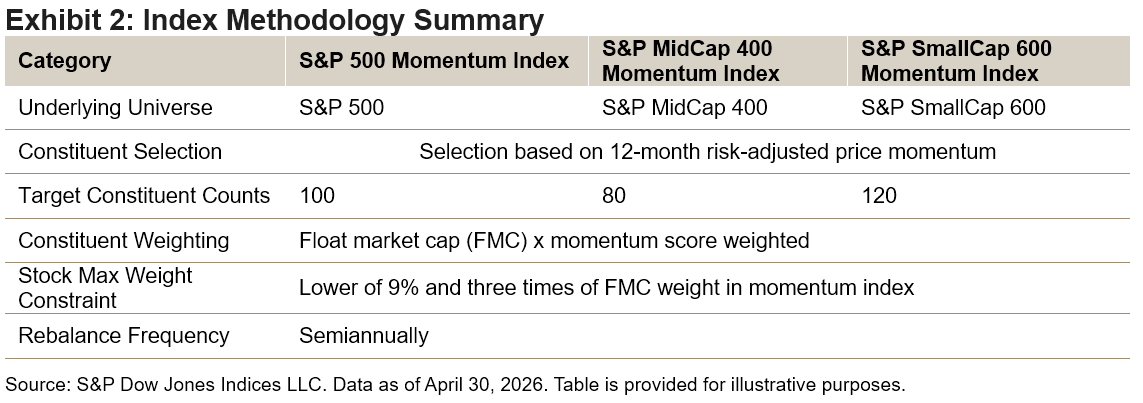

The S&P Momentum Indices typically utilize 12-month risk-adjusted price momentum to select stocks ranked in the top quintile of their eligible universes (see Exhibit 2).1 To account for short-term reversal effects, the most recent month is excluded when calculating price momentum.2 Employing risk-adjusted momentum instead of raw price momentum may help mitigate the negative impacts of idiosyncratic risk associated with raw momentum and can also reduce downside risks.3

The constituents of the S&P Momentum Indices are weighted by the product of their FMC and momentum score, subject to individual security and sector weight constraints. This approach effectively balances market weight with targeted factor exposure. The indices are rebalanced semiannually, with a 20% buffer rule to help reduce turnover.

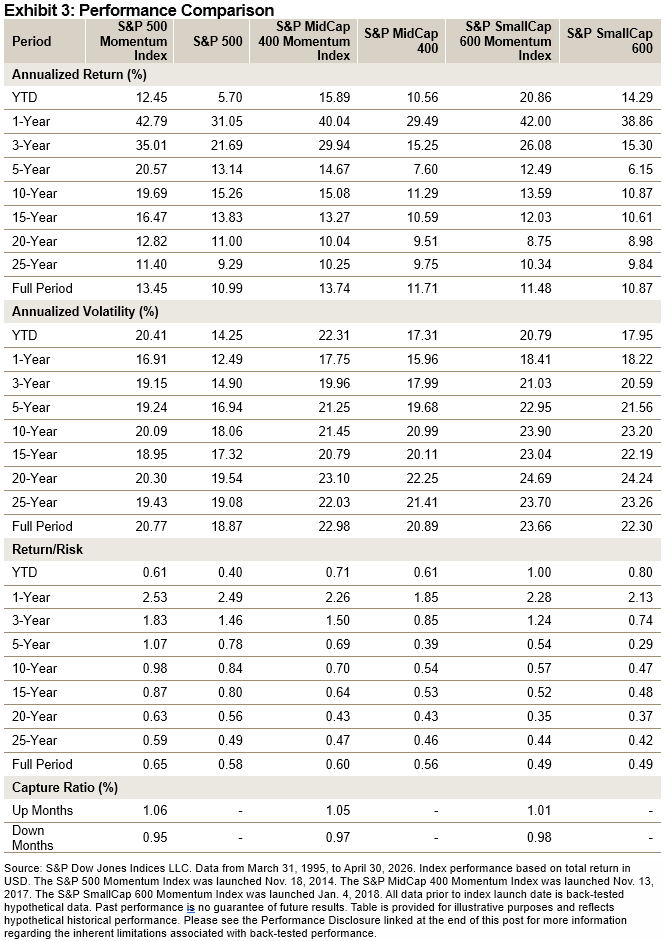

A Short- and Long-Term View of Performance

Exhibit 3 demonstrates that all three S&P Momentum Indices have historically outperformed their respective benchmarks based on both absolute and risk-adjusted returns, in both the short and long term.

Over the past year, the S&P 500 Momentum Index, S&P MidCap 400 Momentum Index and S&P SmallCap 600 Momentum Index outperformed their benchmarks by 11.74%, 10.55% and 3.14%, respectively.

Furthermore, these indices have shown favorable capture ratios, delivering higher or similar gains during up markets4 and experiencing smaller declines during down markets.

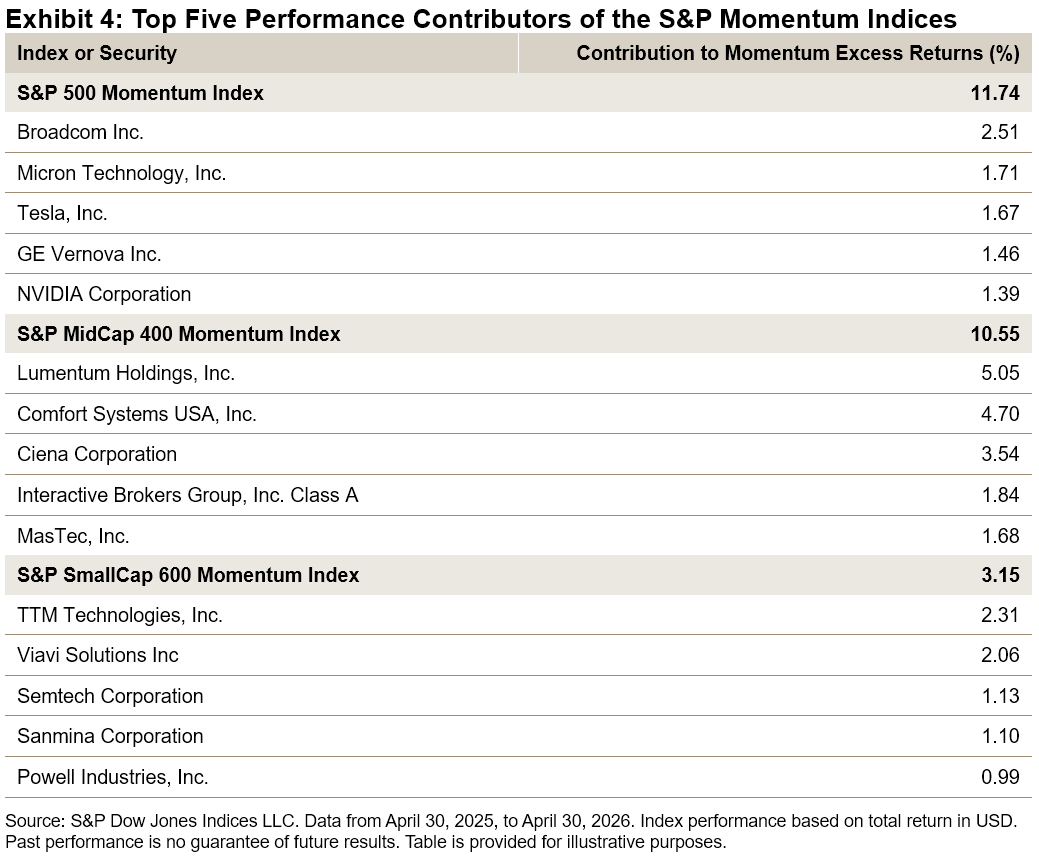

Top Performance Contributors

Exhibit 4 highlights the top five contributors to the performance of these three S&P Momentum Indices over the one-year period ending April 30, 2026. Broadcom, Lumentum and TTM Technologies were the leading performers in the S&P 500 Momentum Index, S&P MidCap 400 Momentum Index and S&P SmallCap 600 Momentum Index, respectively.

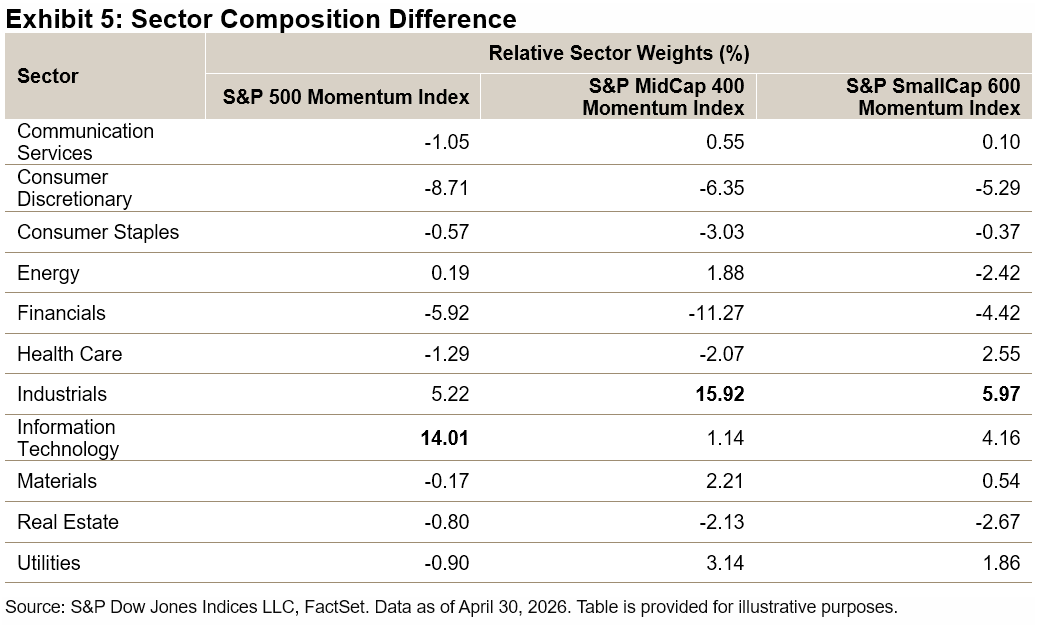

Sectors

Exhibit 5 displays the active sector weights for the S&P Momentum Indices as of April 30, 2026. The S&P 500 Momentum Index overweighed the Information Technology sector by 14.01% relative to the S&P 500. Within the Information Technology sector, it was notably overweight in the Semiconductors and Semiconductor Equipment industry group by 20.61% and underweight in the Software and Services industry group by 7.29%. The S&P MidCap 400 Momentum Index and S&P SmallCap 600 Momentum Index held overweight positions of 15.92% and 5.97%, respectively, in the Industrials sector. All three indices exhibited large underweights in the Consumer Discretionary and Financials sectors.

Conclusion

The April rally underscored the resilience of the S&P Momentum Indices. Their strong performance, driven by a robust risk-adjusted methodology and favorable sector weights, highlights their potential as a systematic approach to reflecting market trends. With their historical outperformance, favorable capture ratios and disciplined rebalancing, these indices provide another tool for navigating the market.

1 Please refer to the S&P Momentum Indices Methodology for more details.

2 Jegadeesh, Narasimhan and Sheridan Titman, “Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency,” The Journal of Finance, Vol. 48, No. 1, March 1993.

3 Fan, Minyou, Kearney Fearghal, Youwei Li and Jiadong Liu, “Momentum and the Cross-section of Stock Volatility,” Journal of Economic Dynamics and Control, Volume 144, November 2022.

4 The market is defined as the monthly performance of the underlying benchmarks from March 31, 1995, to April 30, 2026.

The posts on this blog are opinions, not advice. Please read our Disclaimers.