Just as Latin American musicians dominated global charts in 2025, the region’s equities delivered quite the performance last year. While markets navigated shifting interest rates and economic transitions, Latin America stood out as a top-performing region worldwide. The S&P Latin America BMI hit a high note, surging by 53.8% for the year, outperforming the S&P Global BMI by 31.8% in U.S. dollar terms.

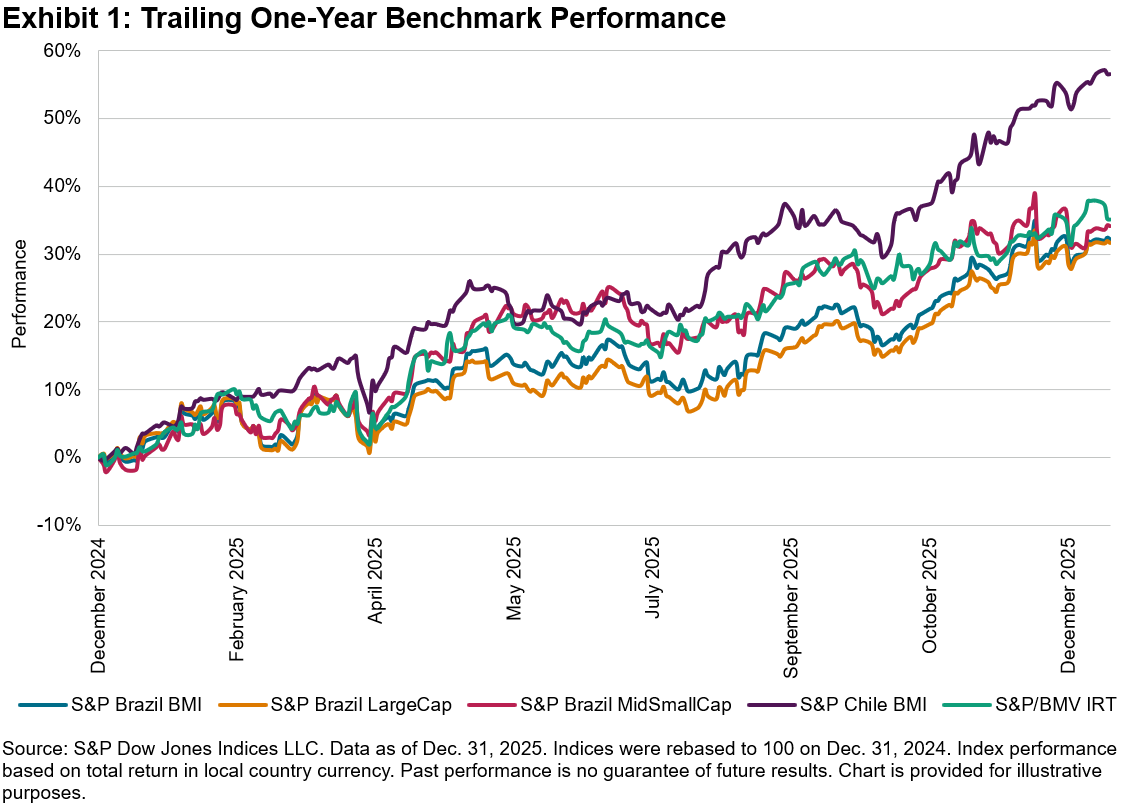

As Exhibit 1 illustrates, this growth was widespread. Chile was the clear standout, with the S&P Chile BMI rising 56.6%, followed by Mexico’s S&P/BMV IRT at 35.2%. Brazil also experienced a robust recovery from its 2024 slump, with the S&P Brazil BMI up 32.2%.

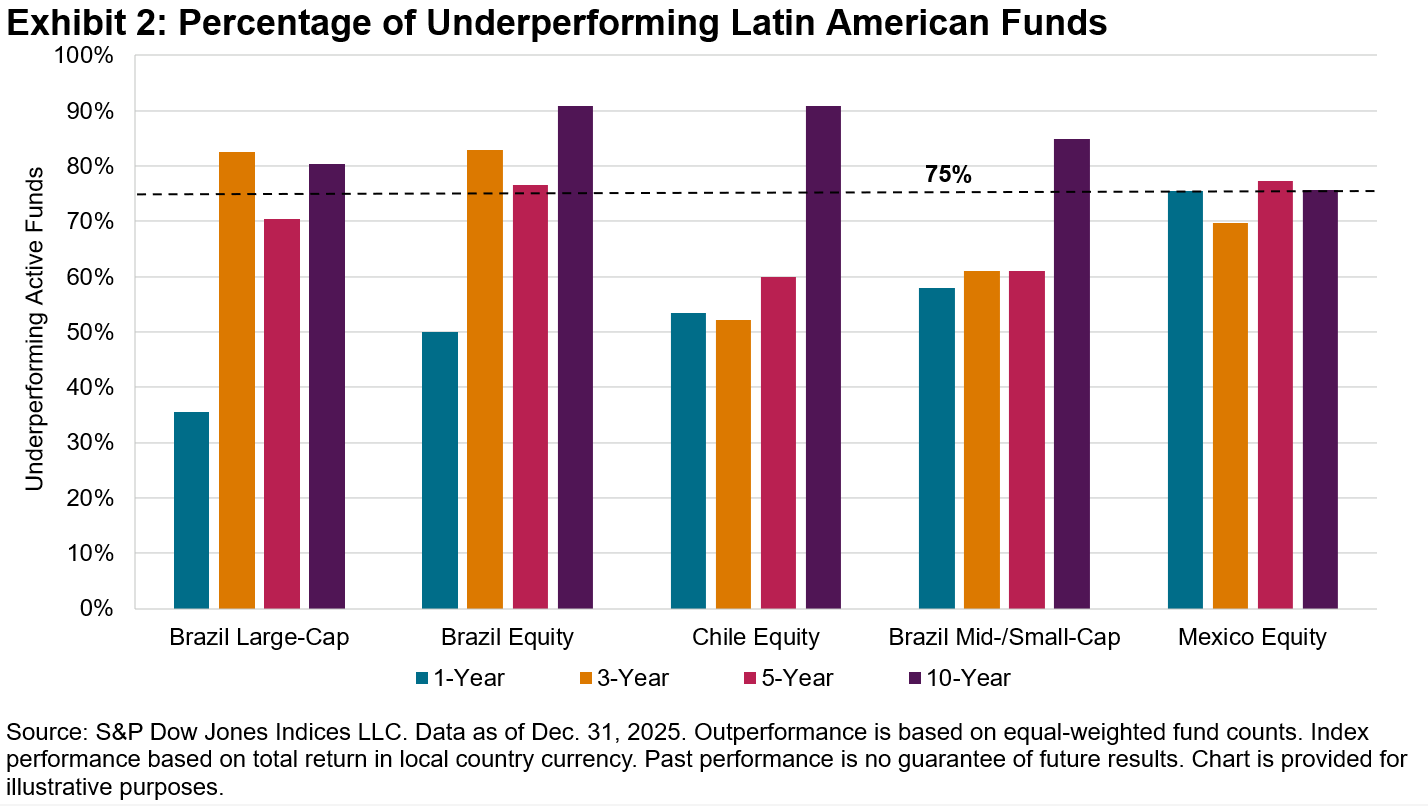

Did active funds sing in tune with the broad rally or end up off-key? The results, detailed in the SPIVA Latin America Year-End 2025 Scorecard, were mixed. While active large-cap equity funds in Brazil fared relatively well, the majority of active funds in all other regional categories failed to capture the full extent of the 2025 surge. As Exhibit 2 shows, over a 10-year horizon, high underperformance (over 75%) remained the undeniable norm across all categories.

To understand why active managers struggled in some countries but succeeded in others in the short term, we can start by looking at market skew and leadership concentration.

In 2025, Latin American markets experienced notable disparities in performance distributions. In Mexico, for example, the S&P/BMV IRT exhibited moderately positive skew. Only 10 stocks (27.0%) outperformed the benchmark, meaning active managers faced a high probability of selecting underperformers. Chile showed a similar, albeit slightly less skewed outcome, with the strongest performers heavily concentrated among the highest-weighted stocks.

Brazil offered a fascinating case study in active management dynamics. While the broader Brazilian equity market saw a relative absence of positive skewness, with over half of its components (51.6%) outperforming the S&P Brazil BMI, the S&P Brazil LargeCap told a different story.

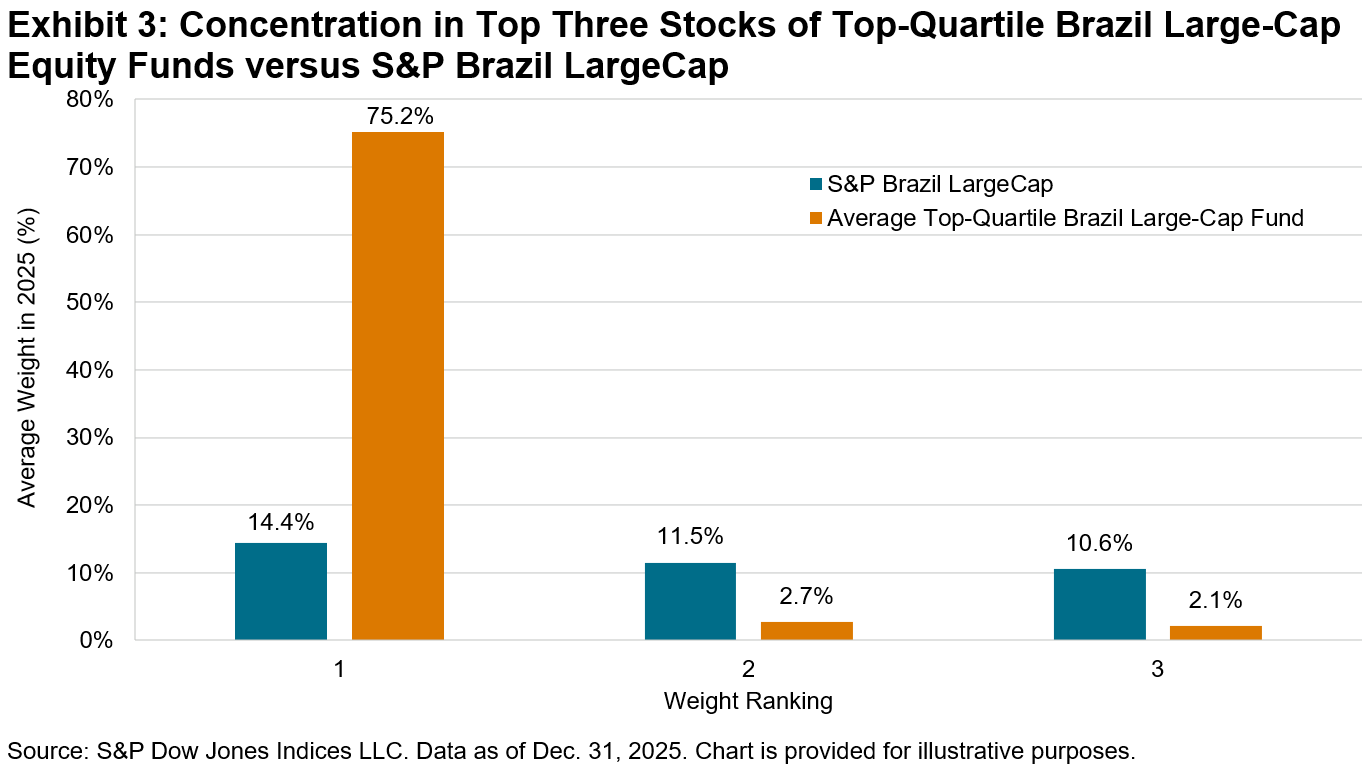

Typically, when a few mega-cap stocks drive a market’s index performance, active funds struggle to keep pace due to portfolio diversification tendencies that shift them away from significant concentration. In 2025, however, Brazil proved to be an exception. Active Brazil Large-Cap funds posted their best results since 2021, aided by highly concentrated positions. While the S&P Brazil LargeCap’s top three constituents accounted for 36.5% of its weight, the average total weight of the top three holdings among top-quartile Brazil Large-Cap equity funds was 80.0%, as shown in Exhibit 3. Perhaps even more remarkably, the average weight of the largest holding in top-quartile Brazil Large-Cap equity funds was 75.2%, illustrating a tilt toward massive single-stock concentration in the pursuit of outperformance.

While riding the momentum of a few large stocks provided a winning ticket for Brazilian large-cap managers in 2025, history serves as a cautionary tale. Relying heavily on a concentrated handful of stocks has carried significant risk when market leadership rotates.

The newly released Latin America Persistence Scorecard Year-End 2025 highlights this exact challenge, answering a critical question: Can these pockets of outperformance be attributed to genuine skill, or are they the result of fleeting luck?

If outperformance were driven by repeatable skill, we would expect it to persist. Instead, the data shows that active management success is overwhelmingly short-lived. Among the 405 funds across Brazil, Chile and Mexico that placed in the top quartile in 2021, a mere 1.2% managed to remain in the top tier over the following four years.

Looking closely at the equity markets, the drop-off was stark. For broad Brazil Equity funds, only 1 out of 81 top-quartile funds from 2021 (1.2%) maintained its status through 2025. In Chile and Mexico, the persistence rate completely vanished; not a single top-quartile equity fund from 2021 maintained its ranking over the subsequent four years.

Furthermore, the data highlighted the possible severe long-term consequences of getting caught on the wrong side of market concentration. Over two consecutive five-year periods, for example, 57.1% of top-quartile Chile Equity funds did not just lose their top-tier status; they fell to the bottom quartile or were liquidated entirely.

Ultimately, 2025 was a record-breaking year for Latin American equities in an absolute sense. Yet, from a relative perspective, the underlying mechanics of skew and concentration proved difficult for most active managers to navigate. The past year may have offered brief pockets of active success in markets like Brazil, but the long-standing results from the SPIVA and Persistence Scorecards continue to remind us that the song remains the same; over the long term, luck has proven fleeting, and consistent outperformance has remained rare.

The posts on this blog are opinions, not advice. Please read our Disclaimers.