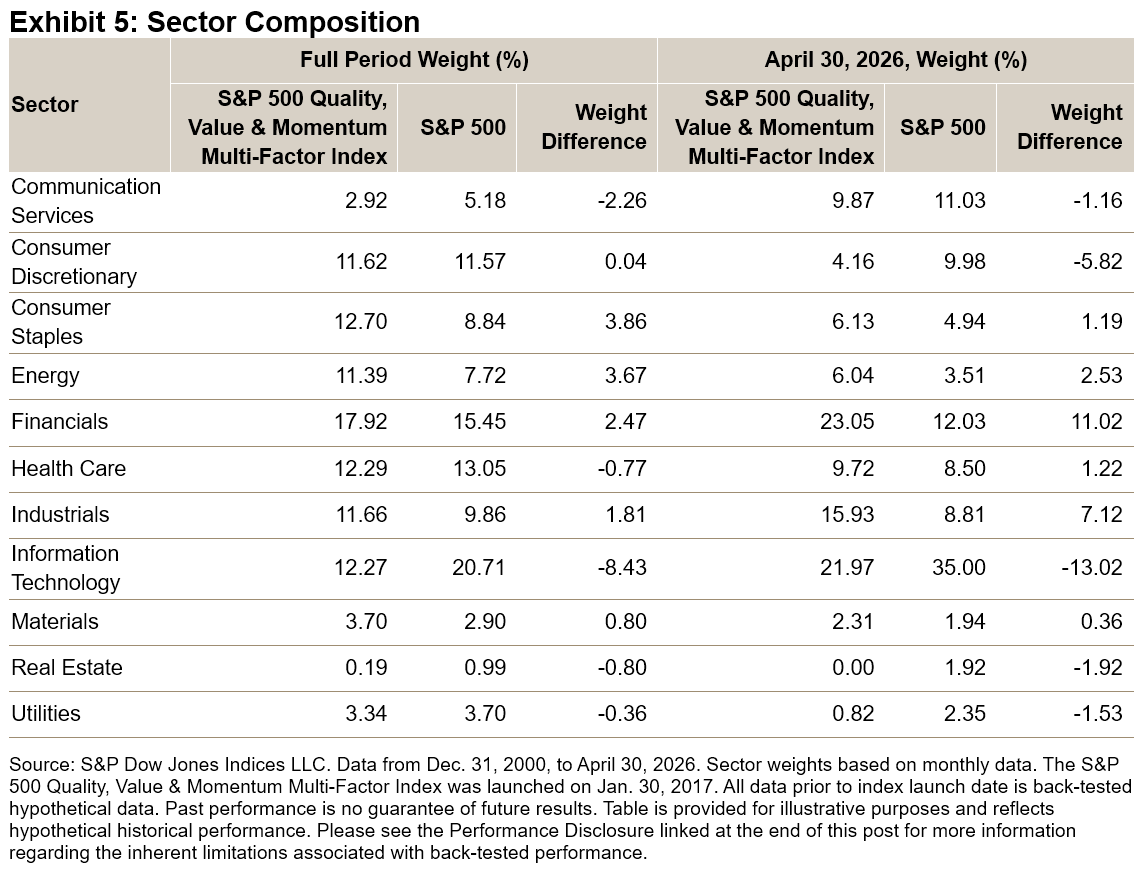

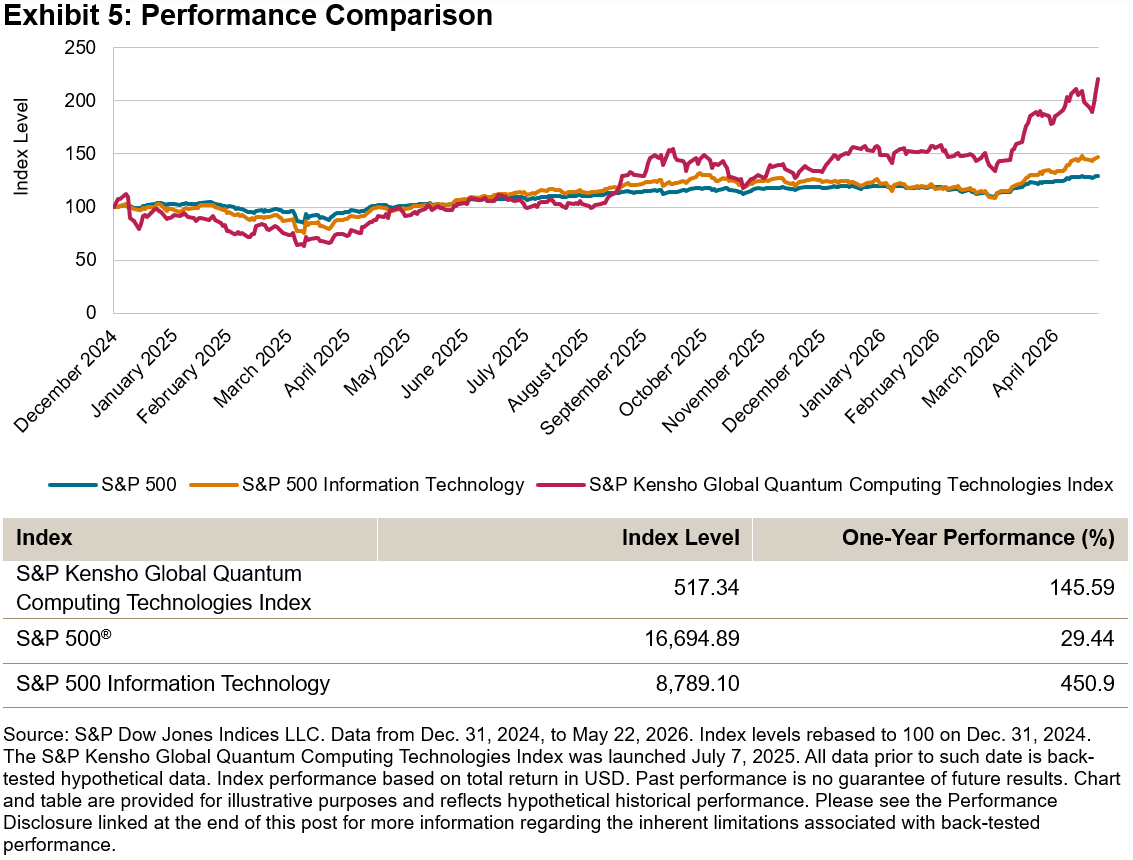

The U.S. government recently committed over USD 2 billion to nine quantum companies under the CHIPS Act,1 taking equity stakes in each. It is a signal that quantum computing has become a matter of national interest. Markets seem to have already been taking note, with the S&P Kensho Global Quantum Computing Technologies Index up 120% since the start of 2025 and 57% quarter-to-date as of May 22, 2026 (see Exhibit 1).

At its core, quantum computing uses qubits. Unlike classical bits that are fixed as either 0 or 1, qubits can exist in a superposition of both states simultaneously until measured. This property makes quantum computers particularly powerful for certain complex problems that are effectively unsolvable by classical computers. The theoretical foundations stretch back decades, but the technology has long been constrained by the difficulty of building stable, error-corrected qubits. In this way, it shares something with AI, where the core ideas preceded the technology needed to make them useful by a generation.

An Index in Motion

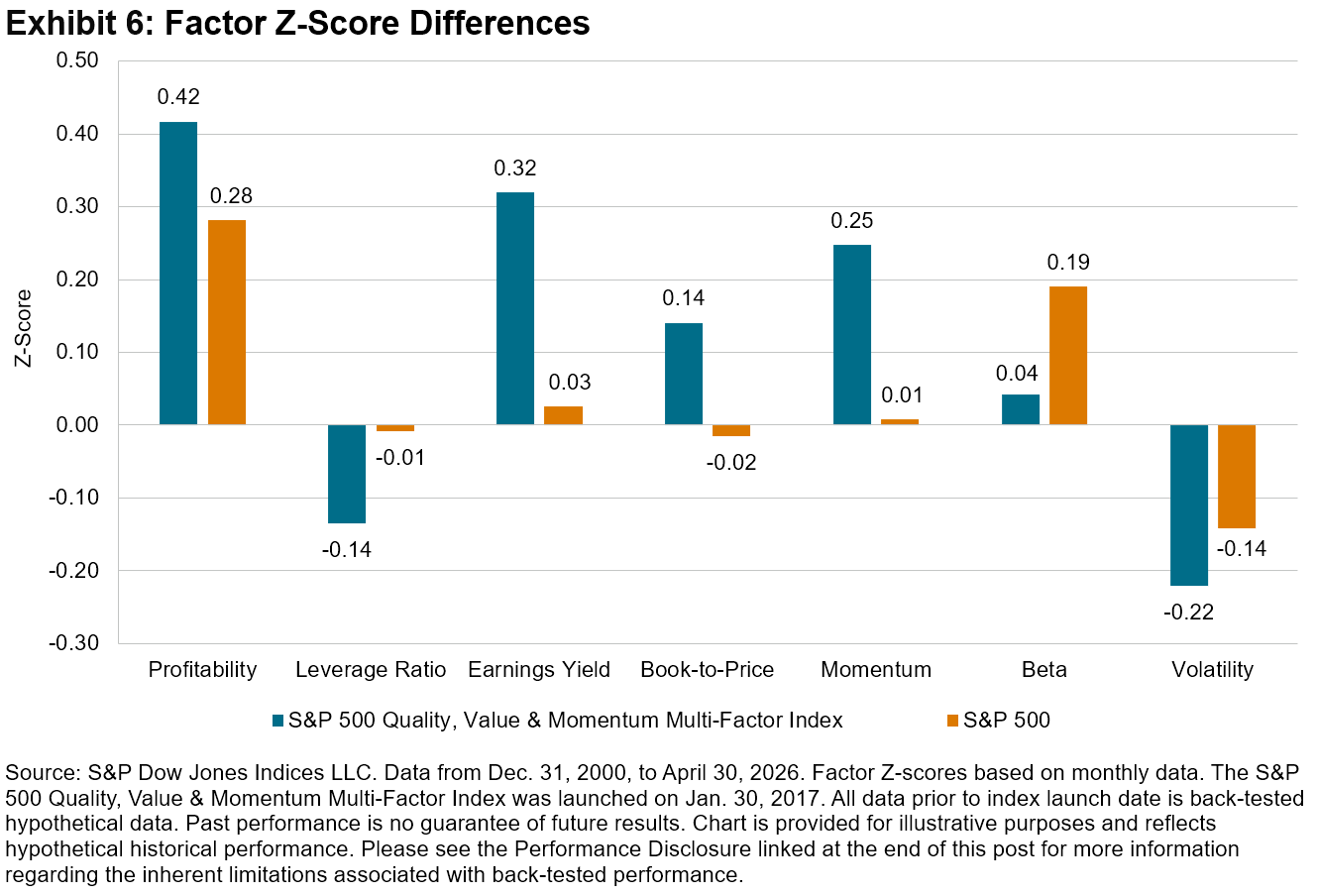

Tracking this fast-evolving space requires a different approach than traditional index construction. As described in a previous blog post, the S&P Kensho Global Quantum Computing Technologies Index uses natural language processing (NLP) to identify relevant companies, rather than relying on standard industry or revenue-based classifications. This matters because most pure-play quantum companies do not yet have tangible recurring revenues, making financial screening alone insufficient. The index has doubled from 13 to 26 constituents between 2022 and 2026, with U.S. companies accounting for 69% of the index’s weight, a concentration that mirrors the dominance of U.S. venture capital in funding quantum research.2

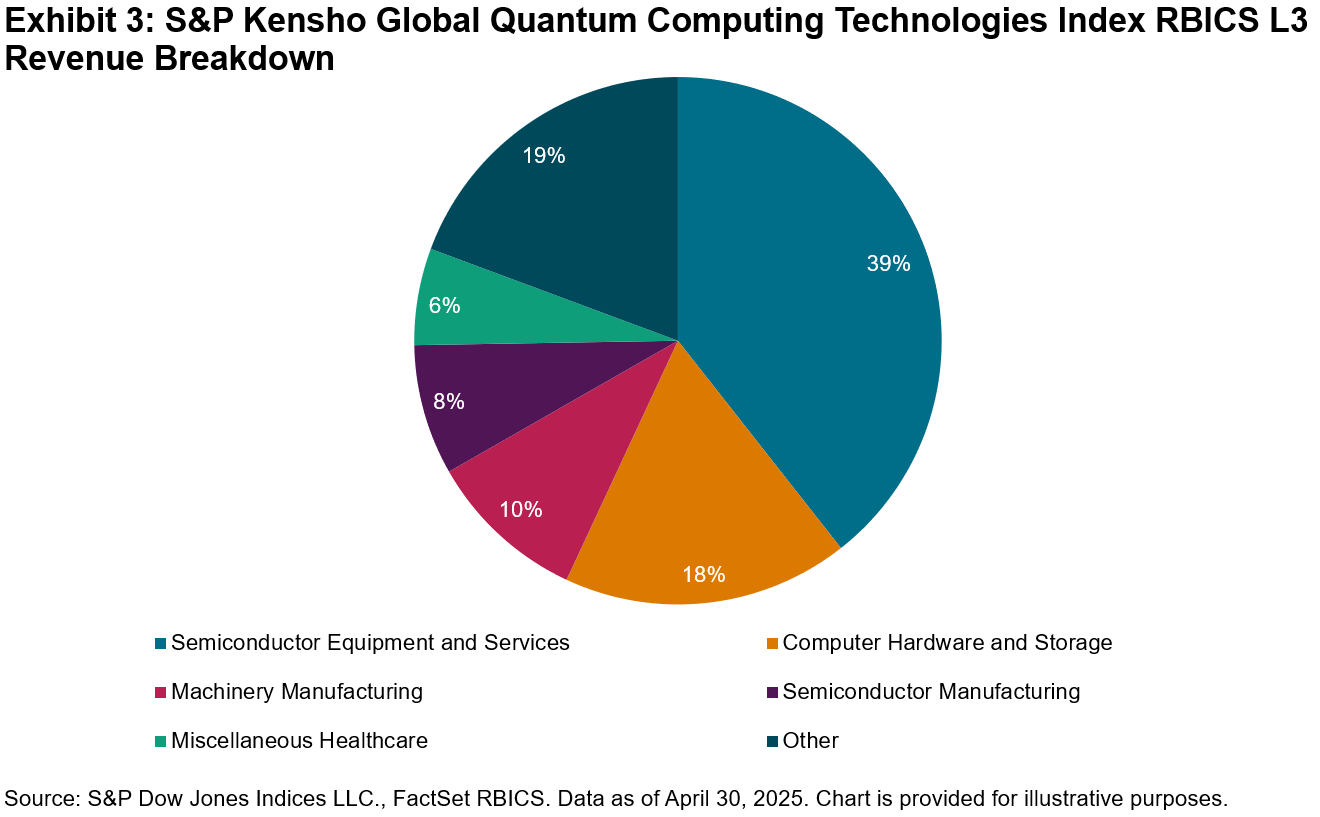

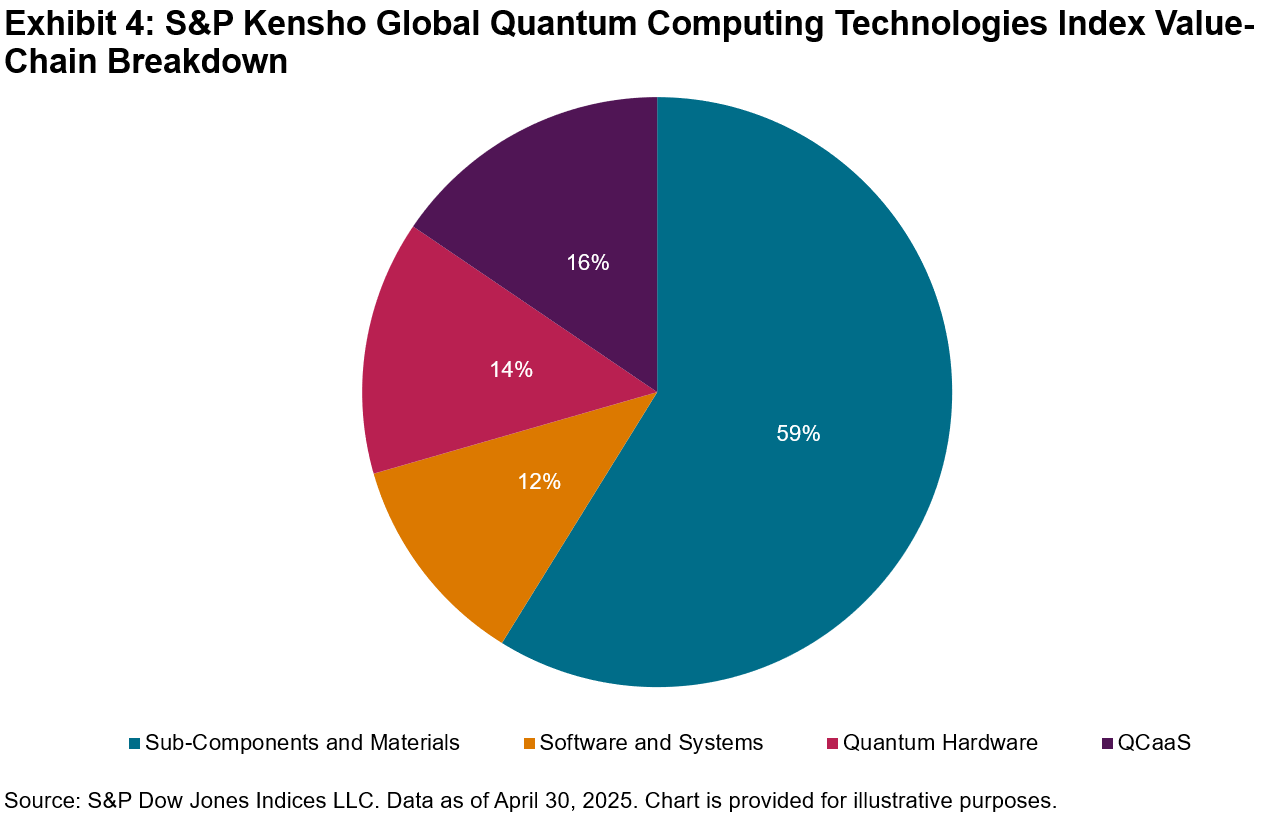

The pie charts in Exhibits 2, 3 and 4 show the breakdown of the S&P Kensho Global Quantum Computing Technologies Index using traditional GICS® industry weights, RBICS revenues and a value-chain analysis, respectively. However, as quantum computing is still a nascent industry, standard approaches still do not reflect it fully.

Since its launched on July 7, 2025, the S&P Kensho Global Quantum Computing Technologies Index is up 107%, but the journey has not been smooth. A significant rally in the September-October 2025 period gave way to a range-bound phase through the end of Q1 2026, before the index accelerated again, adding 57% quarter-to-date as of May 22, 2026. Gains have been broad based, with 22 out of 27 constituents contributing positively to one-year performance (see Exhibit 5).

The Backstage Winners

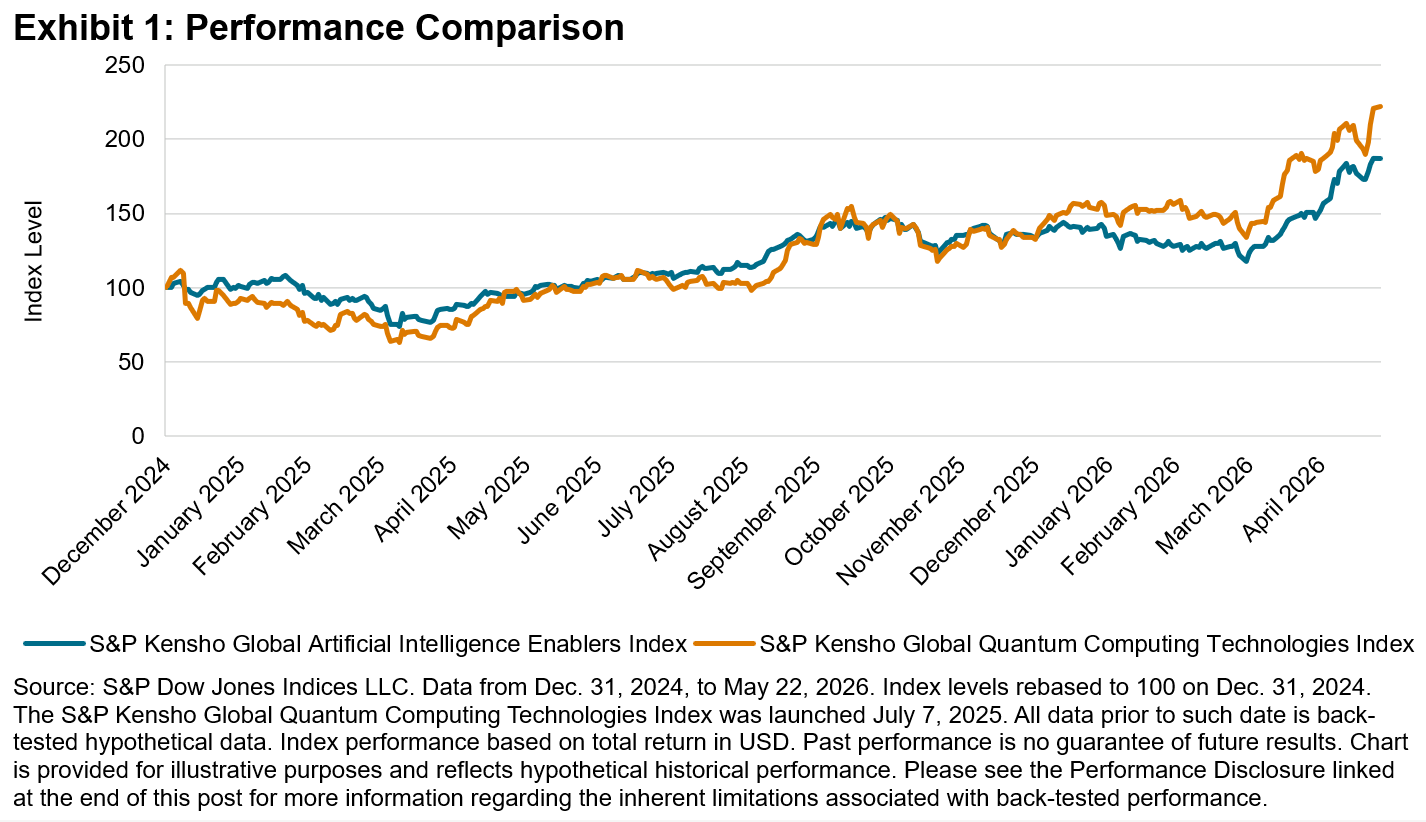

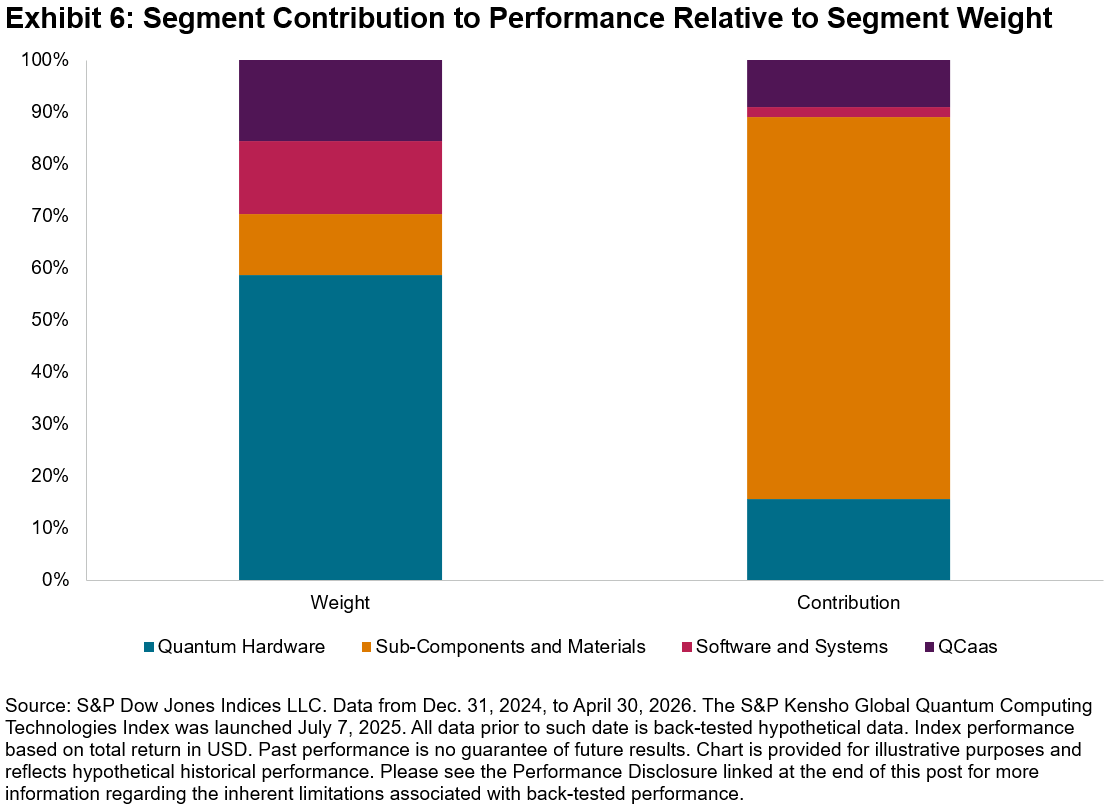

Of the top 10 S&P Kensho Global Quantum Computing Technologies Index contributors, 7 belong to the Sub-Components and Materials segment. As shown in Exhibit 6, this segment represents only 12% of the index’s weight yet has accounted for 73% of overall performance. Quantum Hardware has dominated the index with a weight of 59% but has contributed only 16% to overall performance.

Much of the public narrative around quantum computing is dominated by QCaaS companies such as D-Wave, Rigetti and IonQ—the companies that are generally considered to be the closest to building real world quantum applications. Yet the strongest returns have come from a less visible part of the ecosystem: the companies supplying the components behind the hardware. For example, Soitec provides silicon on insulator wafers critical for advanced chip design;3 FormFactor provides semiconductor test and measurement equipment;4 while Coherent supplies optical components and specialty fiber used in AI data center infrastructure and quantum hardware.5 Each of these companies carries quantum exposure on top of an already strong underlying business tied to AI infrastructure spending, something pure-play quantum names cannot yet claim.

This reflects where quantum computing stands today, still in the infrastructure building phase. The more downstream companies, the QCaaS names and those closest to real world applications, remain more directly tied to the longer-term potential of the technology.

Quantum’s Present Tense

Quantum computing’s story is not waiting to start.6 In cryptography, researchers and government agencies have begun flagging a risk7 known as “harvest now, decrypt later,” where malicious actors collect encrypted data today with the intention of decrypting it once quantum computers are powerful enough to break current encryption standards. It is a threat that is already informing how some governments and enterprises think about long-term data security.

The S&P Kensho Global Quantum Computing Technologies Index will continue to measure the evolution of this technology. Its performance across segments, from Sub-Components to QCaaS, offers a window into how the technology itself is progressing and which stage of the quantum journey is leading the market at any given time.

1 National Institute of Standards and Technology, “Department of Commerce Announces Letters of Intent With 9 Companies for $2 Billion to Accelerate U.S. Leadership in Quantum Computing,” May 21, 2026.

2 Ruane, J., Kiesow, E., Galatsanos, J., Dukatz, C., Blomquist, E., Shukla, P., “The Quantum Index Report 2025,” MIT Initiative on the Digital Economy, Massachusetts Institute of Technology, Cambridge, MA, May 2025.

3 Soitec, “Semiconductors Fabs: Speed and time-to-market acceleration – A global presence.”

4 FormFactor, “Press Release,” May 13, 2026.

5 Coherent, “Specialty Optical Fibers.”

6 Hopkins, Brian, “Practical Quantum Computing By 2030 Is Likely — And So Is Q‑Day,” Forrester, March 11, 2026.

7 Mascelli, Jillian and Rodden, Megan, “‘Harvest Now Decrypt Later’: Examining Post-Quantum Cryptography and the Data Privacy Risks for Distributed Ledger Networks,” Board of Governors of the Federal Reserve System, September 2025.

The posts on this blog are opinions, not advice. Please read our Disclaimers.