In the previous webinar wrap-up, we discussed the manager perspective; here, we take a look at the allocator perspective and the index provider response to a maturing market and the institutional market’s requirements for better benchmarks.

The ETF Effect: Bitcoin Beta Has Become Cheaper

If Bitcoin is an imperfect benchmark, it remains an unavoidable one for a different reason: it may now be considered the clearest expression of cheap, accessible crypto beta.

Chris Solarz framed the issue from the allocator’s perspective. For him, benchmarking is the prerequisite for identifying alpha, because outperformance only has meaning relative to a credible alternative. And that alternative has changed materially since the arrival of spot Bitcoin ETFs. Solarz noted that Bitcoin exposure can now be obtained at low cost—he cited fee competition driving ETF pricing down to as little as 14 bps.1

That has major implications for active managers. If investors can access core crypto beta passively and cheaply, then the justification for paying hedge fund-style fees rests on true excess return, not simply exposure to a rising market. Solarz put it plainly: the only thing investors should pay for is alpha. If net returns are not above what could have been achieved through a passive index or ETF, then the value proposition of active management becomes difficult to defend.

This is one of the webinar’s most important institutional takeaways: the commoditization of beta is leading to more precise conversations about what active crypto managers actually do. That is healthy for the market, but it may raise the bar considerably.

A More Segmented Way to Measure Crypto Funds

Solarz’s solution is not to abandon broad reference points, but to use a more segmented framework. When evaluating liquid digital asset managers, he starts with four benchmarks:

This approach recognizes that digital assets are not one homogeneous pool of risk. Bitcoin remains the dominant reference asset; Ethereum reflects a distinct smart-contract and ecosystem; Solana increasingly represents another major asset and the remaining altcoin universe requires its own lens.

This framework helps allocators ask sharper questions. Is a manager outperforming because they generated security selection alpha? Because they made a successful allocation call across crypto subsegments? Or because they simply maintained exposure to the best-performing beta bucket?

Solarz was also candid that no single framework fully resolves the issue. Institutional committees will still ask the obvious question: why not just own Bitcoin? That remains a fair opportunity-cost benchmark, especially for investors starting from zero. But he argued that relying on Bitcoin alone may do an injustice to the complexity of the asset class, where sectors such as DeFi, payments, gaming, metaverse and other subsectors can behave very differently.

In other words, Bitcoin may still be a starting point, but it may no longer be the end of the conversation.

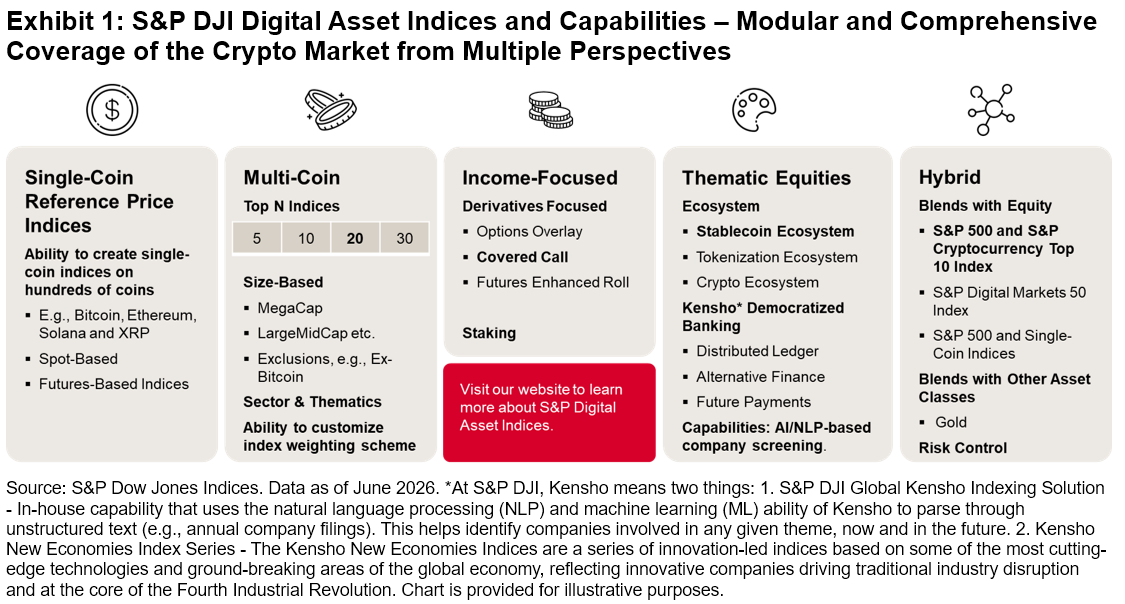

Why Building Indices in Crypto Is Harder than It Looks

Rounding out the discussion with the index provider’s perspective, S&P Dow Jones Indices (S&P DJI) approaches the market through several lenses: single-coin indices, multi-coin strategies, crypto-linked equity indices and hybrid cross-asset benchmarks that blend digital assets with traditional asset classes.

Even apparently simple questions like the following can become complex in this market.

- How should the price of a single token be constructed?

- Which exchanges should be used in the pricing methodology?

- What qualifies as large cap, mega cap or broad market in crypto?

- Should an index be purely market-cap weighted, equal weighted, capped or filtered?

- How should benchmark construction adapt as market concentration changes over time?

Index names alone never tell the full story. Methodology matters. Definitions matter. And in a market as dynamic as crypto, those definitions can change quickly as market structures evolve. At S&P DJI, we offer a range of digital asset solutions for different market objectives.

Learn more about our capabilities and view the full webinar replay.

1 As of the time of the webinar. For more information, please see Daodu, Sam, “Bitcoin News: Morgan Stanley Just Launched the Cheapest Bitcoin ETF on the Market,” Yahoo Finance, April 11, 2026.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

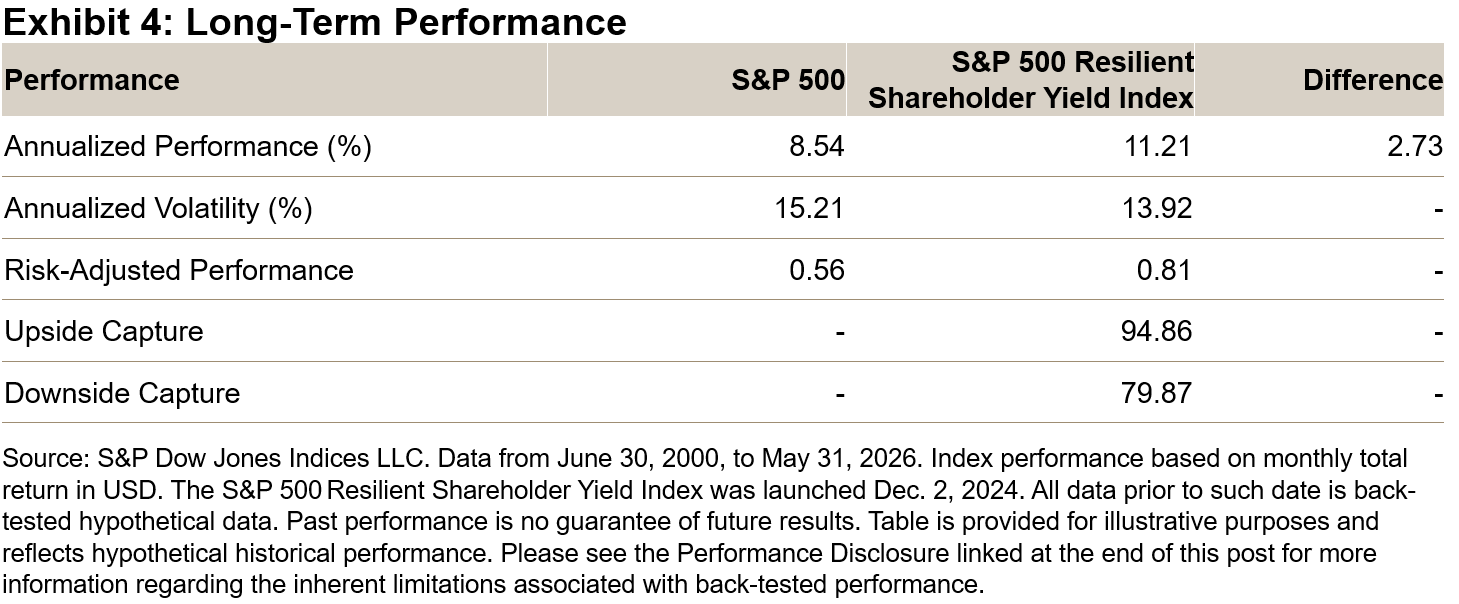

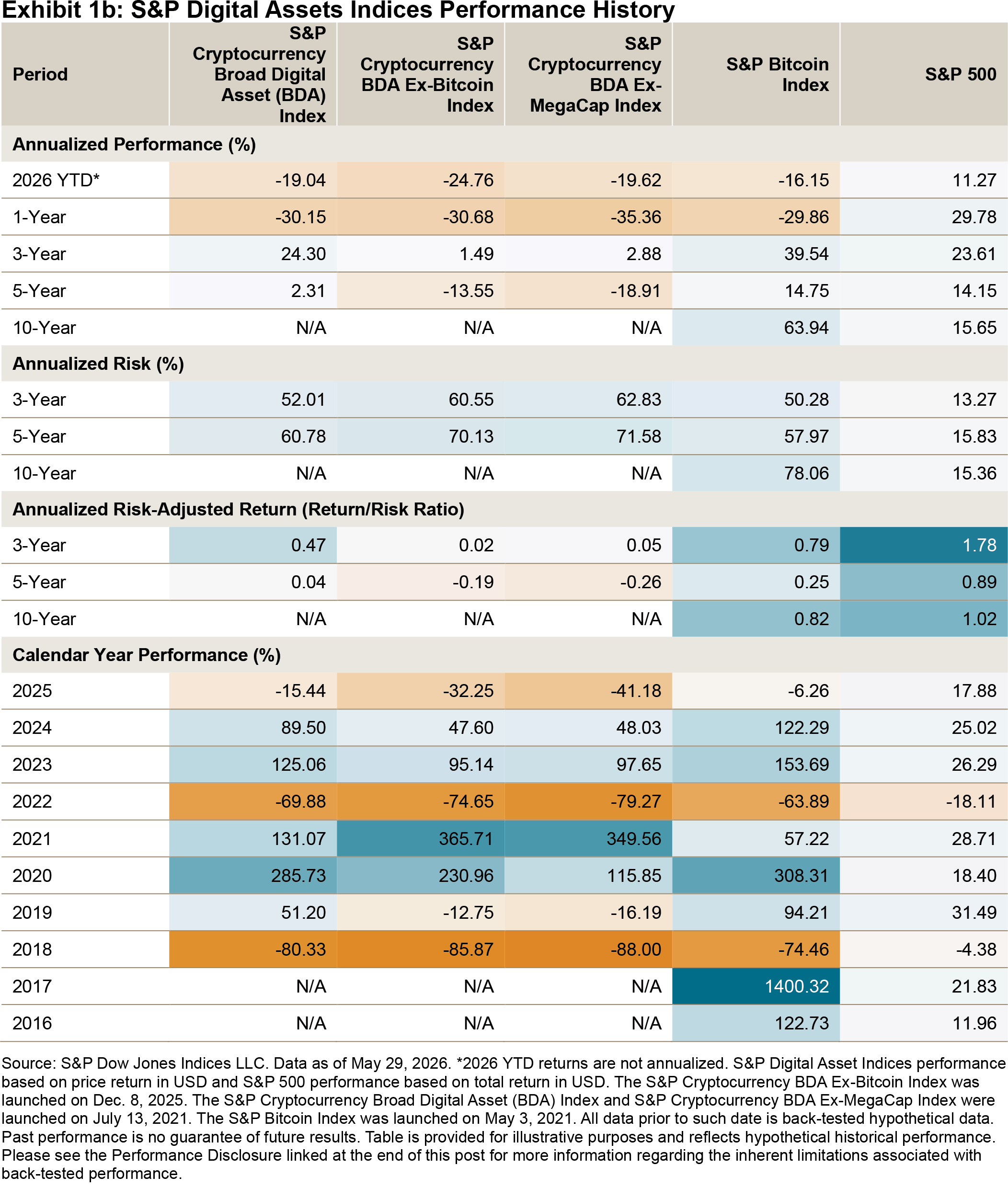

Long-Term Performance Characteristics

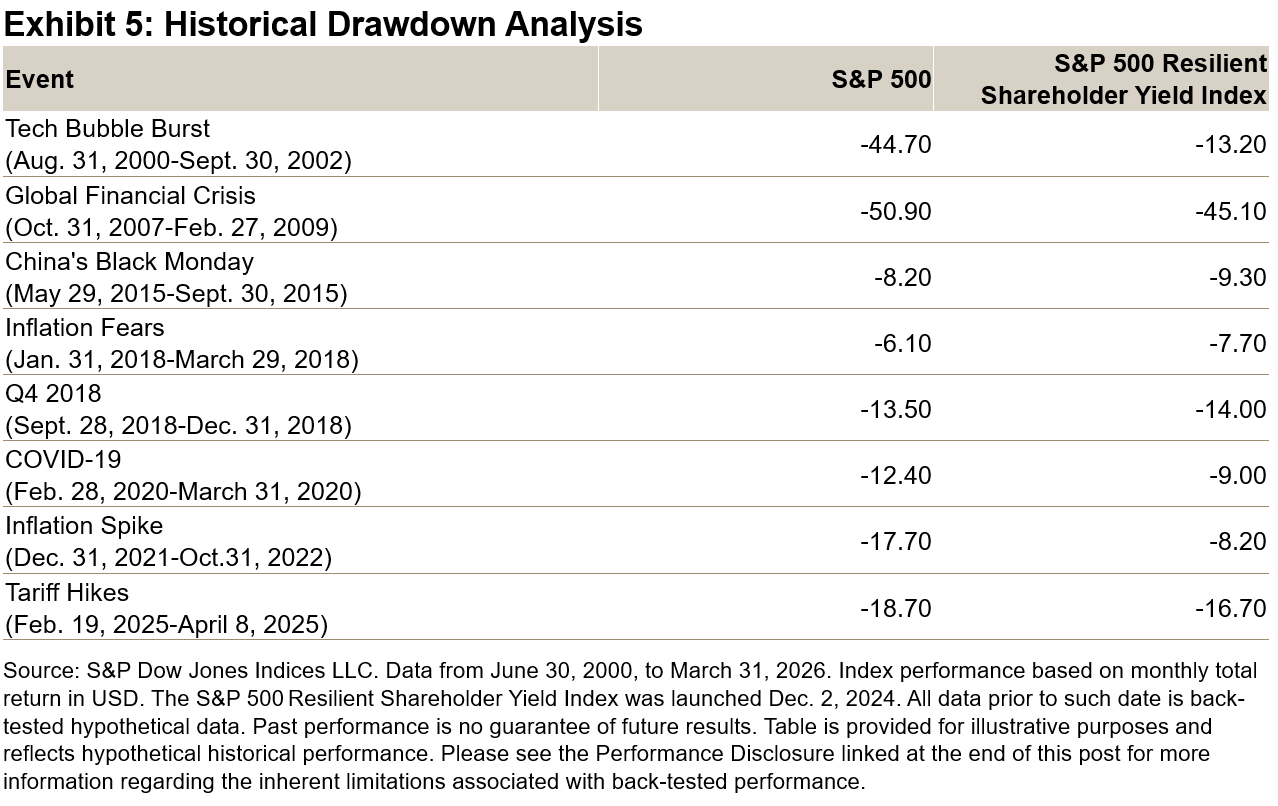

Long-Term Performance Characteristics