The Crypto Ecosystem and Digital Asset Index Landscape

As digital assets continue to move into the institutional mainstream, investors are increasingly looking for ways to gain exposure to the space in a holistic way that considers all parts of the crypto value chain, from equities to digital assets. The S&P Digital Markets 50 Index is a hybrid benchmark that combines listed companies tied to the crypto ecosystem with direct exposure to major digital assets. This cross-asset approach provides broader access to the blockchain economy than digital assets alone.

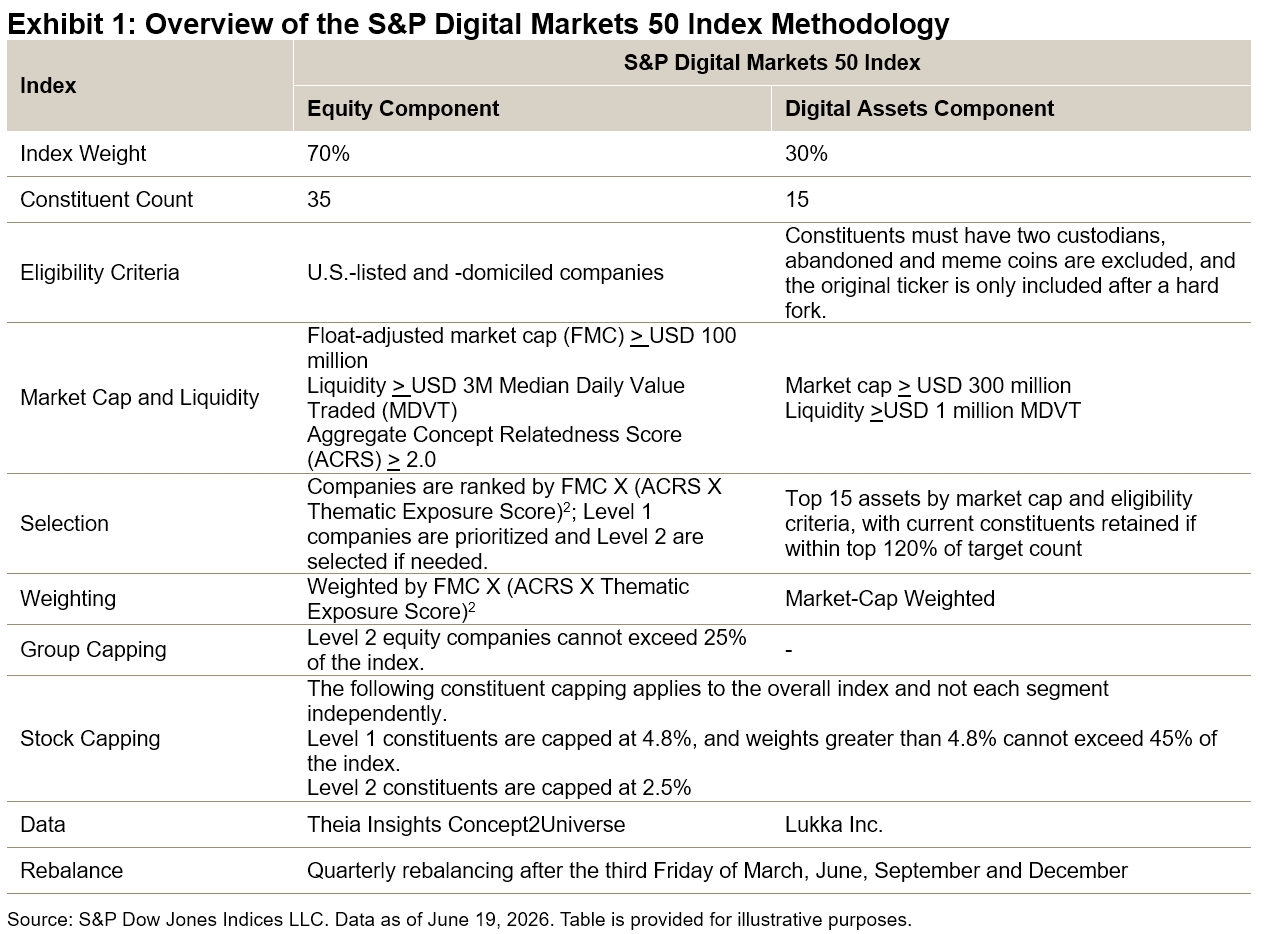

Methodology of the S&P Digital Markets 50 Index1

Looking at how the index is constructed, the equity portion constitutes 70% of the index and is made up of 35 U.S.-listed and -domiciled public companies from the S&P Global BMI that are involved in crypto and digital asset infrastructure (operators, infrastructure providers, financial services, blockchain applications and supporting technologies). These companies build the infrastructure and services that are central to the digital transformation, spanning areas including exchanges, custody, payments, on-ramps, analytics, hardware and institutional rails.

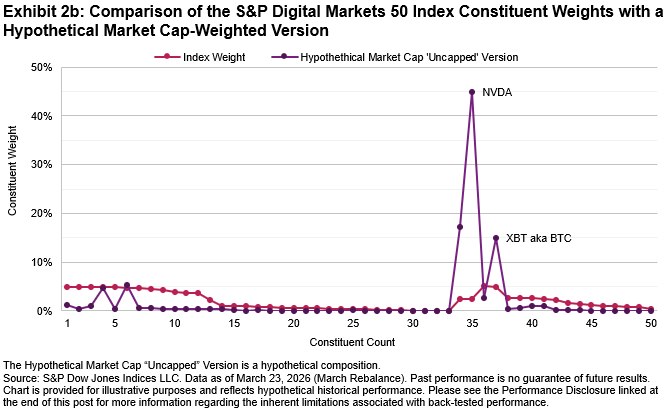

The digital assets portion comprises 30% of the index and is made up of 15 cryptocurrencies selected from the S&P Cryptocurrency Broad Digital Asset (BDA) Index. The inclusion of native protocols and assets like Bitcoin highlights the latter’s status in the crypto market as the largest asset, often given the moniker “digital gold.” Ethereum and Solana represent the use of protocols as Layer 2 networks and platforms, where much of the infrastructure for tokenization and trading is being built. Bitcoin and Ethereum are categorized as Level 1 crypto assets and individually capped at 5%, while all other crypto assets in the index are individually capped at 2.5%.

At the heart of the index is having a mixed representation of constituents and striking a balance between the equity and digital asset components, while also considering the weights of companies that are highly related to the crypto ecosystem (which we refer to as Level 1) and those that are somewhat related and contribute to the theme (which we refer to as Level 2). Level 1 companies with higher crypto ecosystem relatedness are capped at 5% to allow weight for other emerging Level 1 companies that may have a lower market cap and support the diversification of the index. Level 2 companies, which may have some involvement in DeFi, but a lower level, are capped at 2.5% at rebalance but have some runway intra-quarter. This can be valuable, ensuring that mega-cap companies like Alphabet (Google) and Nvidia—which have some involvement in crypto—do not dominate the index compared as they may with a market cap-weighted approach.

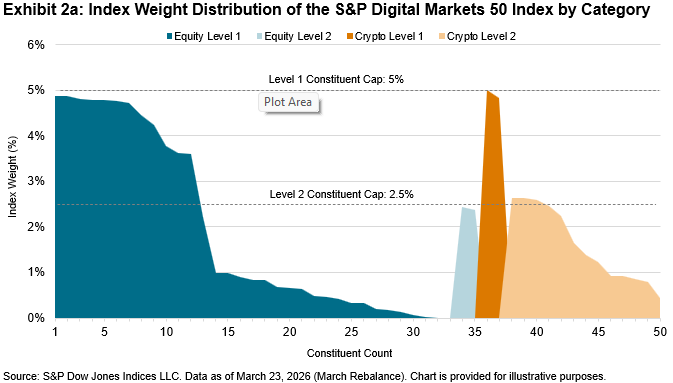

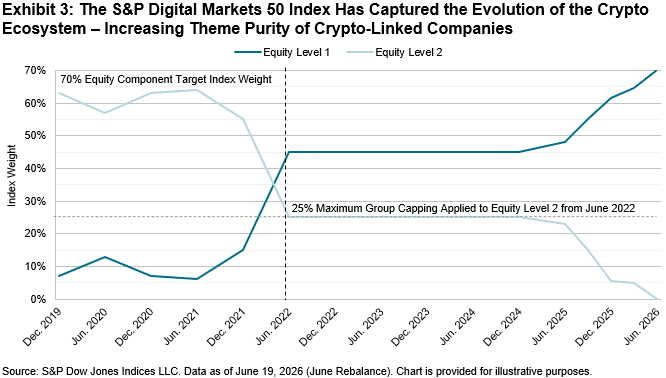

With the growing number of crypto-related companies, the index’s equity component dropped Nvidia and Google during the June rebalance, with the theme purity of the equity segment increasing over time. As the crypto ecosystem develops, the “purity” of companies represented in the S&P Digital Markets 50 Index has increased over time when looking at changes to the composition of Level 1 and Level 2 companies, as shown in Exhibit 3.

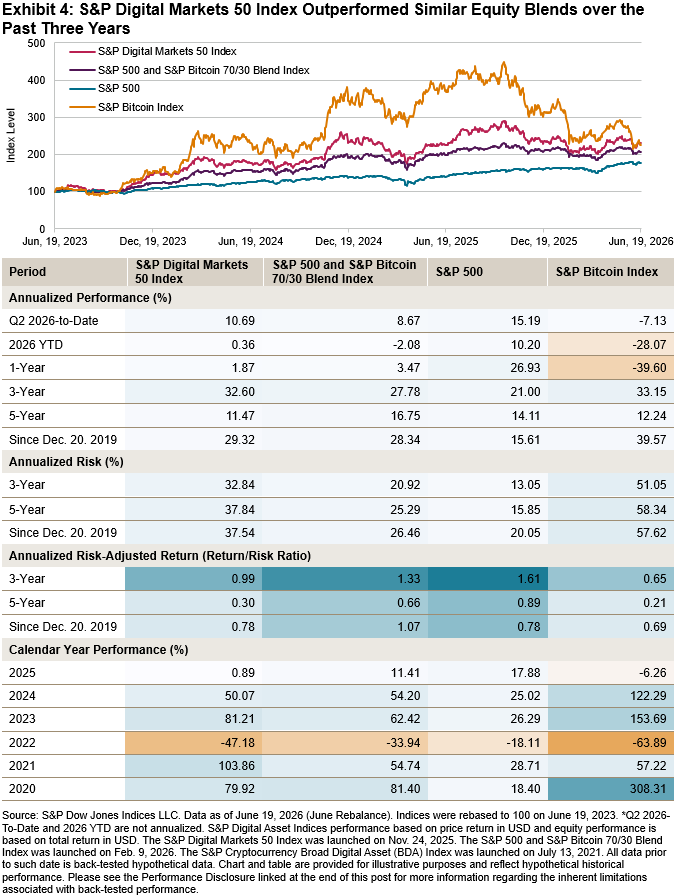

Performance of the S&P Digital Markets 50 Index Compared to Relevant Benchmarks

The S&P Digital Markets 50 Index provides market participants with a view of some of the upside capture of the crypto market and characteristics of the equity market, with a lower downside versus pure crypto assets. For example, in 2022, the S&P Digital Markets 50 Index declined 15% less than the standalone S&P Bitcoin Index, which saw a downside of 64%. In 2021, the S&P Digital Markets 50 Index outperformed both the S&P 500 and the S&P Bitcoin Index, demonstrating the potential tailwinds that can occur when both crypto-linked equities and the digital assets universe beyond crypto are outperforming.

When compared to a similar multi-asset index—the S&P 500 and S&P Bitcoin 70/30 Blend Index—the S&P Digital Markets 50 Index outperformed over various time periods, including 2026 YTD, the three-year horizon, and since the index’s first value date on Dec. 19, 2019.

For market participants with a strong interest in the future of digital assets and the crypto ecosystem, the S&P Digital Markets 50 Index could serve as a useful measure of this dual approach across equities and digital assets.

To learn more about the index, please see the S&P Digital Markets 50 Index brochure.

1 Please see the S&P Crypto Ecosystem Index Methodology for the full details, such as constraint relaxation, turnover mitigation rules and corporate action treatment.

The posts on this blog are opinions, not advice. Please read our Disclaimers.