In this blog, we introduce the Dow Jones Commodity Index 3 Month Forward – Quarterly Reweight (DJCI 3MQT). Launched in August 2025, the DJCI 3MQT is a variant of the Dow Jones Commodity Index (DJCI). The DJCI 3MQT has historically outperformed the S&P GSCI and the Bloomberg Commodity Index (BCOM): over the 10-year period ending June 30, 2026, the DJCI 3MQT outperformed the S&P GSCI by 175 bps and the BCOM by 330 bps.

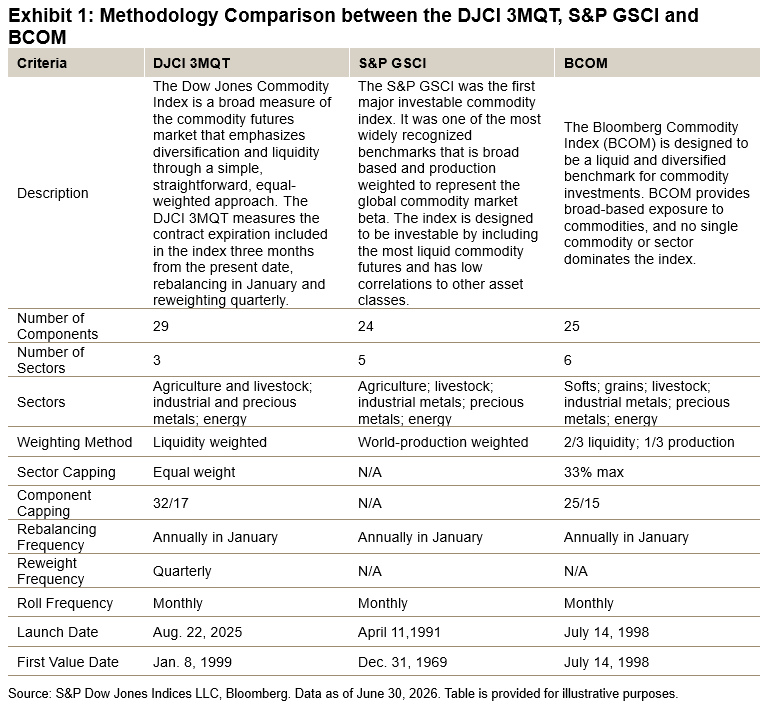

As of its January 2026 reconstitution, the DJCI 3MQT includes 29 commodity futures contracts, representing global commodities across three sectors: agriculture and livestock; energy; and metals. Like the S&P GSCI and BCOM, the DJCI 3MQT holds the front-month futures contract, rolls monthly and rebalances annually in January.

Unlike the S&P GSCI and BCOM, the DJCI 3MQT is liquidity weighted and reweights quarterly. Additionally, the DJCI 3MQT caps the maximum weight of any commodity component at 32%, with any remaining commodity components capped at 17%, and equally weights between commodity sectors. These weighting constraints are applied iteratively until all requirements are met.

Exhibit 1 shows a methodology comparison between the DJCI 3MQT, S&P GSCI and BCOM.1

Let’s explore how the DJCI 3MQT’s three unique methodology components—emphasis on liquidity, equal weighting between sectors and quarterly rebalancing—have historically enhanced performance and reduced volatility.

Emphasis on Liquidity

By emphasizing liquidity, the DJCI 3MQT offers a unique measurement of the commodities market. Liquidity, which is proxied by the total dollar value traded for constituent commodities, determines the weight and, therefore, the importance of the constituents within the index.

As commodities are real assets, it’s difficult for commodity producers to quickly change production or storage capacity to meet changes in demand. In contrast, financial market participants, such as hedgers and speculators, can quickly change their trading behavior to meet changes in demand. As such, the liquidity of commodities contracts, rather than their production data, more accurately mirrors the real-time importance of individual commodities.

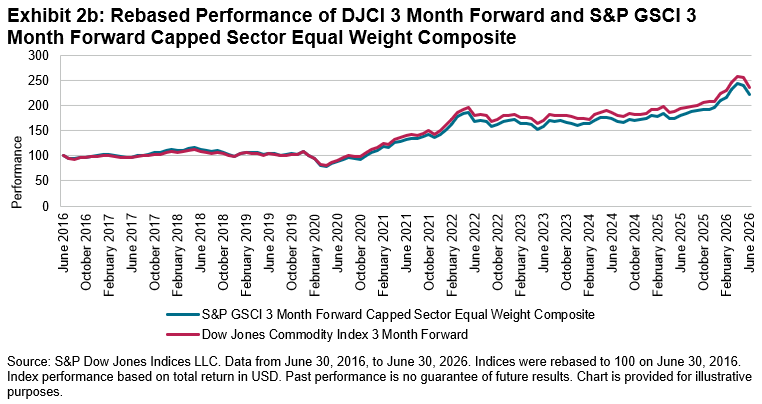

The historical effect of liquidity on index performance is clear. In Exhibit 2, we compare the Dow Jones Commodity Index 3 Month Forward (DJCI 3M) against the S&P GSCI 3 Month Forward Capped Sector Equal Weight Composite.2 These two indices are methodologically the same, other than the choice between liquidity or production. As of June 2026, the DJCI 3M had outperformed the S&P GSCI 3 Month Capped Sector Equal Weight Composite by 69 bps on a 10-year basis.

Equal Weighting between Sectors

Next, we turn to the second characteristic of the DJCI 3MQT—enhanced diversification. Compared to the S&P GSCI and BCOM, the DJCI 3MQT has historically had higher diversification through its overall constituent count (29 versus 24 and 25, respectively),3 as well as through its unique equal-weighted approach to commodity sectors and concentration limits on individual commodities.

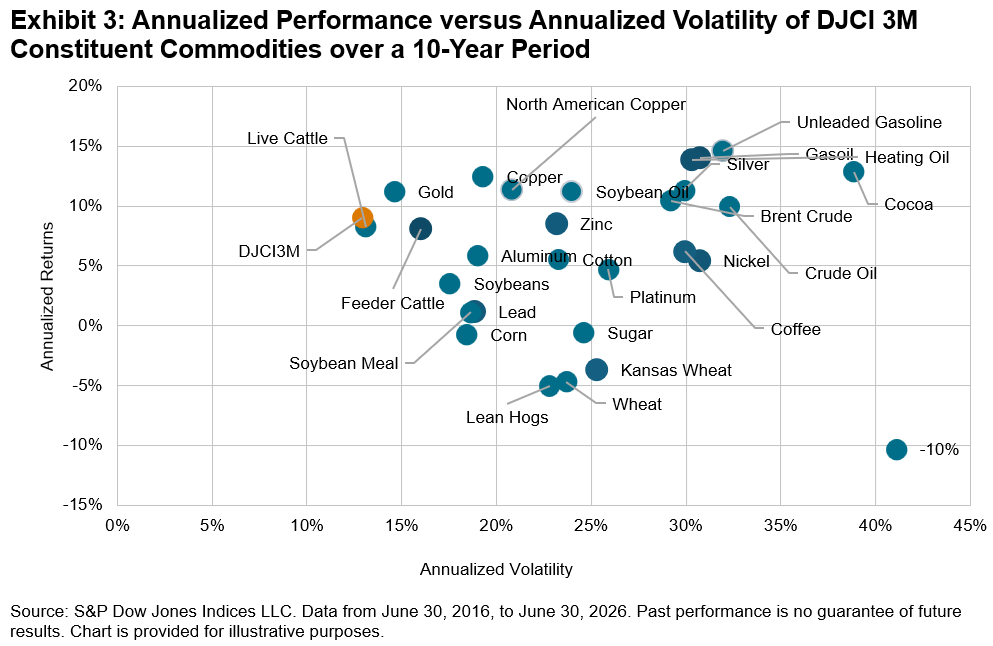

The effect of being highly diversified is demonstrated in Exhibit 3, which graphs the annualized performance against the annualized volatility of the DJCI 3M and its constituent commodities over the past 10 years.4 The DJCI 3M achieved higher annualized performance while exhibiting lower annualized volatility compared to its constituent commodities.

As of June 2026, the 10-year weighted average annualized performance of the DJCI 3M constituent commodities was 7.1%, and the 10-year annualized performance of the DJCI 3M was 9.0%. The 10-year weighted average annualized volatility of DJCI 3M constituent commodities was 23.9%, and the 10-year annualized volatility of the DJCI 3M was 12.9%. This demonstrates the essence of modern portfolio theory—that diversification may be the only “free lunch” in investing—as the DJCI 3M has both increased annualized performance and decreased annualized volatility compared to its individual constituents.

More Frequent Reweighting

Finally, we turn to the third characteristic of the DJCI 3MQT’s methodology: more frequent reweighting. The DJCI 3MQT reweights quarterly to its annual January rebalance weights. This reweighting enables the index to adhere to its intended, liquidity-based weights.

Without the quarterly reweight, the effective U.S. dollar weights of the constituent commodities float based on price changes; this unintentionally adds a momentum component to the index. However, commodities are often mean reverting, such that a momentum strategy can underperform.

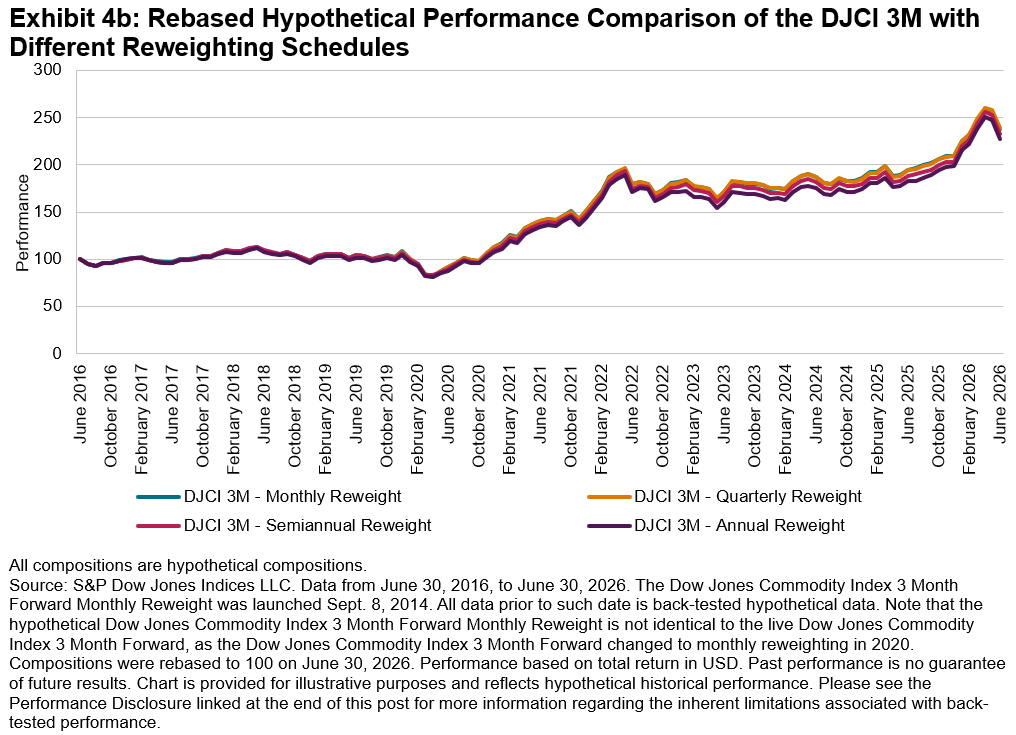

A potential positive effect of a more-frequent reweighting strategy is shown as a comparison in Exhibit 4, which outlines the performance of hypothetical compositions of the DJCI 3M with different reweighting schedules: monthly, quarterly, semiannually and annually. As of June 2026, the quarterly reweight version of the DJCI 3M outperformed the annual reweight (i.e., no reweight) version by 55 bps over the 10-year period.

For further reading, please see Why DJCI? and Dow Jones Commodity Index 3 Month Forward: A Simple Strategy to Measure Enhanced Roll Yield.

1 For more information, please see the Dow Jones Commodity Index Methodology.

2 There is no exact S&P GSCI corollary for the DJCI 3MQT, therefore the DJCI 3M is used as a proxy to isolate the impacts of liquidity weighting.

3 As of the indices’ respective January 2026 reconstitution

4 DJCI 3MQT single constituent commodities are not readily available. Therefore, the analysis in this exhibit is proxied with the DJCI 3M.

The posts on this blog are opinions, not advice. Please read our Disclaimers.